The Bridge between Stablecoins & Fintech Credit

Share Now:

More than 70% of founders think debt is what you take when you’ve run out of cash.

In reality, debt is what you take to scale your venture efficiently.

When it comes to DeFi, most investors think T-Bills (Treasury Bills) are the only safe source of yield left, but there is a much bigger picture here.

For decades, TradFi has pushed for private credit deals, due to their positive nature of risk-adjusted returns, DeFi is yet to fully realize the potential of low-risk, high-yield opportunities that come with lending to real-world fintech borrowers with verifiable onchain infrastructure.

Here’s how both sides win.

Debt isn’t a sign of weakness - it’s a sign of maturity

Whether you have $1 million or $100 million in the bank, your ability to access credit is what truly determines how quickly you can move beyond your balance sheet.

Early-stage fintechs that secure even a small $100K-$1M line - yes, at higher initial rates (~18% ROI) - are buying more than money: they’re buying a repayment track record that compounds credibility for future scalability.

When your business later needs $10M+ in structured debt, that record is what opens doors.

There’s no difference between having $1 million or $100 million in your bank, your ability to access credit really defines how fast you can move beyond your balance sheet.

Sure, early-stage fintechs secure small credit lines ($100k - $1m) at higher rates (~18%).

But they aren’t just buying money, they are buying their future scalability.

Lenders don’t fund ideas, VCs do that.

Lenders fund patterns of repayment.

When your business booms and you need $10 million in structured debt, your repayment record is what opens doors, not your MVP.

Why sitting on cash isn’t a growth strategy (obviously)

If a fintech with millions in the bank avoids building debt relationships early, it’s signaling one of two things:

either it doesn’t expect exponential growth, or it doesn’t understand how debt amplifies equity.

When growth accelerates, idle cash gets deployed fast - and you won’t be earning T-Bill yields anymore.

At that point, no lender will instantly sanction multi-million-dollar unsecured loans.

Banks, especially, lend only to those with a history.

Fintechs that start small now - build repayment discipline - stay ahead in the future.

You don’t create credit relationships when you’re desperate; you create them when you’re optional.

Let’s take an established fintech company, holding millions in the bank but not taking debt relationships.

This signals one of two things

1) The business doesn’t expect exponential growth and has hit a plateau

2) The business doesn’t understand how debt amplifies equity

Assuming this business ends up growing, its idle cash is quickly exhausted and suddenly there is no T-Bill yield.

At this juncture, no lender or bank is going to instantly sanction multi-million dollar unsecured loans to someone with no credit history.

Bank credit isn’t perfect

Yes, banks do provide low-cost capital, but with strict prerequisites:

You must hold a business bank account with them.

Most early facilities are secured - loans against cash collateral or fixed deposits.

Without a relationship, banks rarely offer unsecured or under - collateralized loans.

They typically need 3 years of audited financials, sustained cash flows, and a proven operational history.

Even then, access depends on relationships and deposits as much as balance sheet size.

So yes, bank capital is cheap - but it’s earned, not granted.

That’s why smart fintechs first build credit history through structured, alternative debt before approaching banks for the best rates possible.

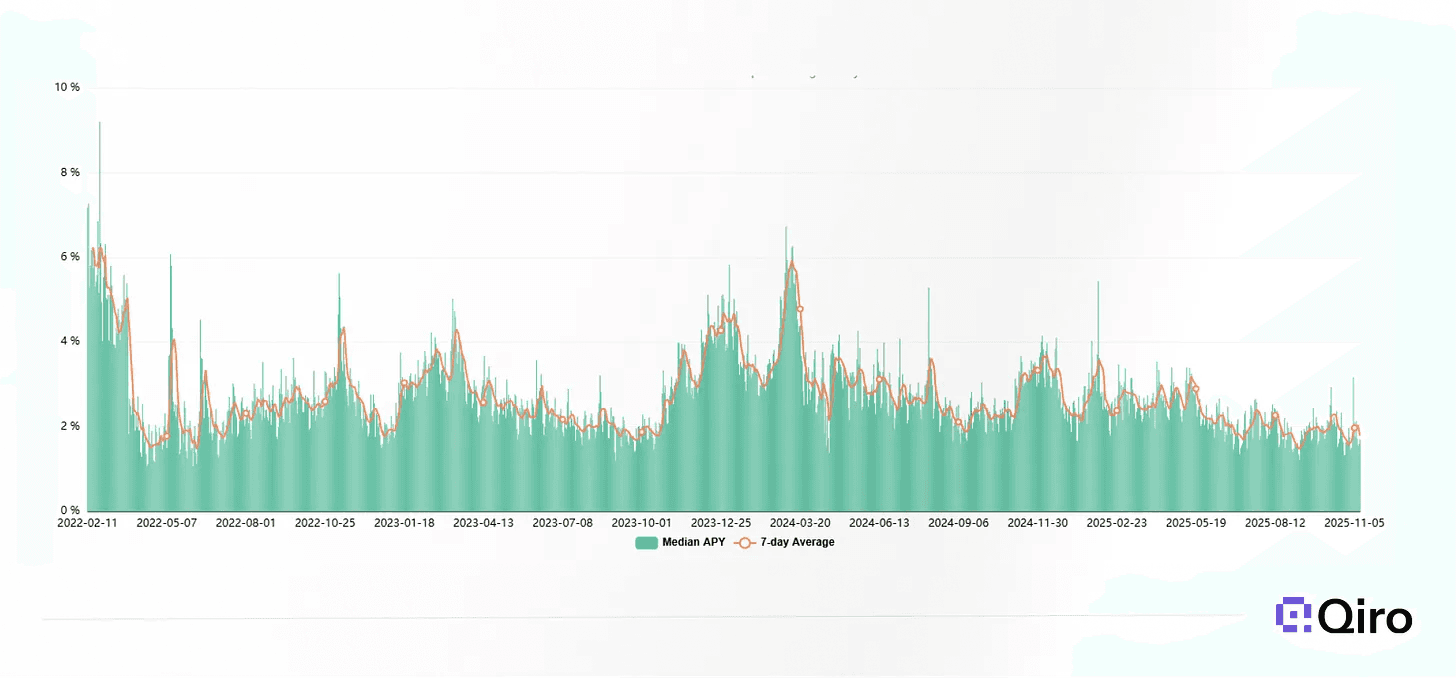

The “risk-free 8%” myth

Let’s get the numbers right.

The only true risk-free yield is 3-4% from short-dated U.S. Treasury bills.

DeFi lending rates of 6-8% (Aave, Morpho, etc.) are not risk-free - they carry protocol, liquidity, and counterparty risk.

Borrowing at 10-12% for productive, secured growth is not expensive - it’s skewed and market-aligned.

Even after such sophisticated strategies, pools and APY claims, the median APY is around ~1.5%, clearly showcasing where investors are deploying their capital. This is the most clear signal that stablecoin investors deserve better portfolio diversification options and if a business yields 15-20% ROI, paying 10-15% for capital still leaves a positive spread - and keeps your equity intact.

Looks like a win for both the stakeholders.

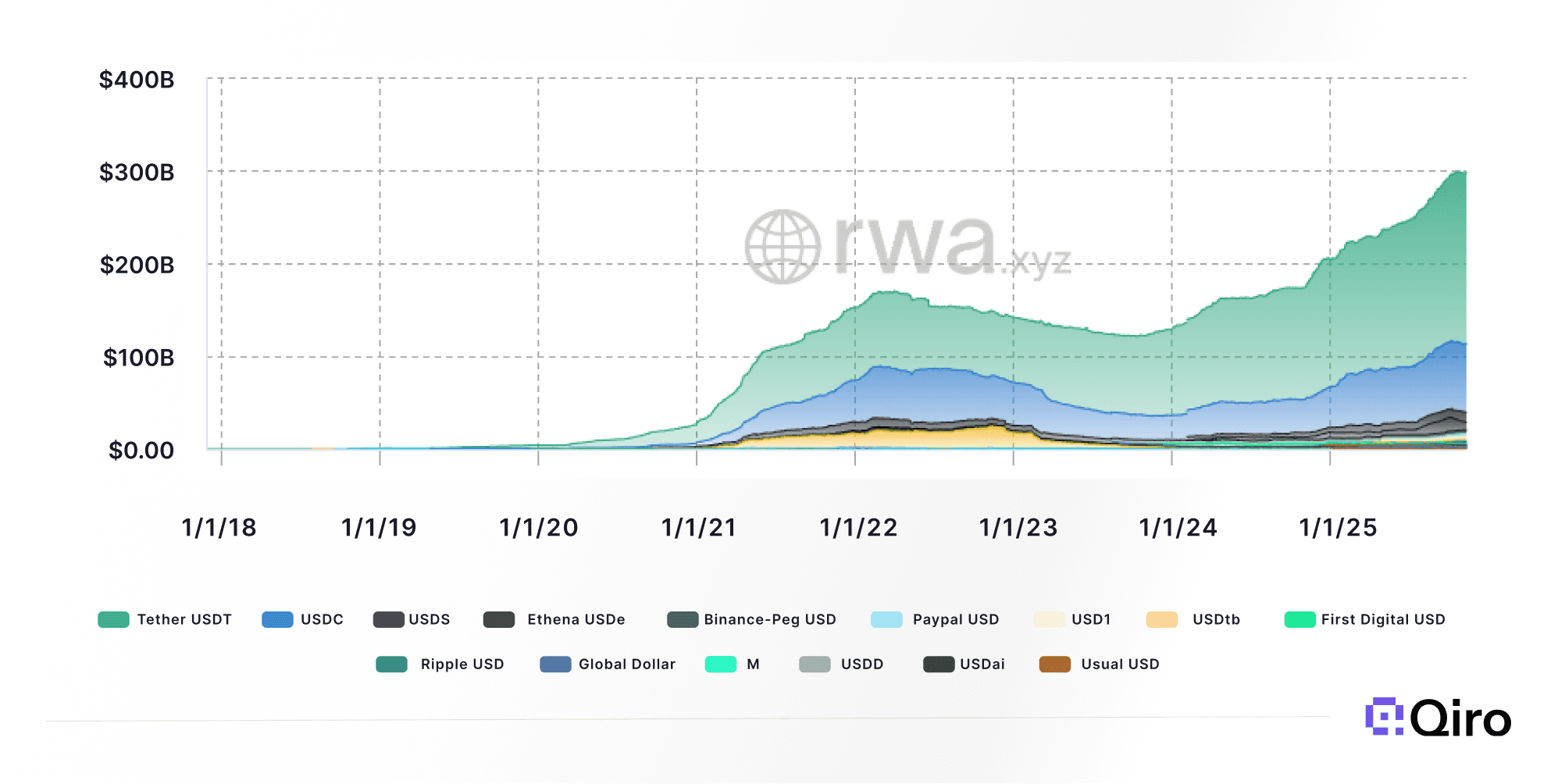

Stablecoins are your venture’s best friend

Stablecoins are now the universal funding rail uniting both Web3-native and Web2-digital fintechs.

The opportunity spread is endless, from cross-border payments, stablecoin cards, remittance players and DePIN networks in Web3 to trade financing, working capital loans and invoice-discounting in Web2.

All of these ventures share the same requirements.

In spite of this demand, stablecoin investors park capital in T-Bills or Tokenized Money Market funds, earning 3-5%

The next obvious step is to deploy a piece of the pie in low-risk, short duration fintech credit offering 10-18% APY, secured and verifiable.

Why I co-founded Qiro

At Qiro we are building the infrastructure that connects stablecoin investors with institutionally underwritten fintech borrowers worldwide - particularly across developed markets like the USA, UK, EU, Singapore, and UAE.

What Qiro does

Identifies qualified fintech borrowers ready for structured capital.

Underwrites risk through a robust, data-driven credit infrastructure.

Tokenizes and distributes these opportunities to stablecoin investors with full transparency and compliance.

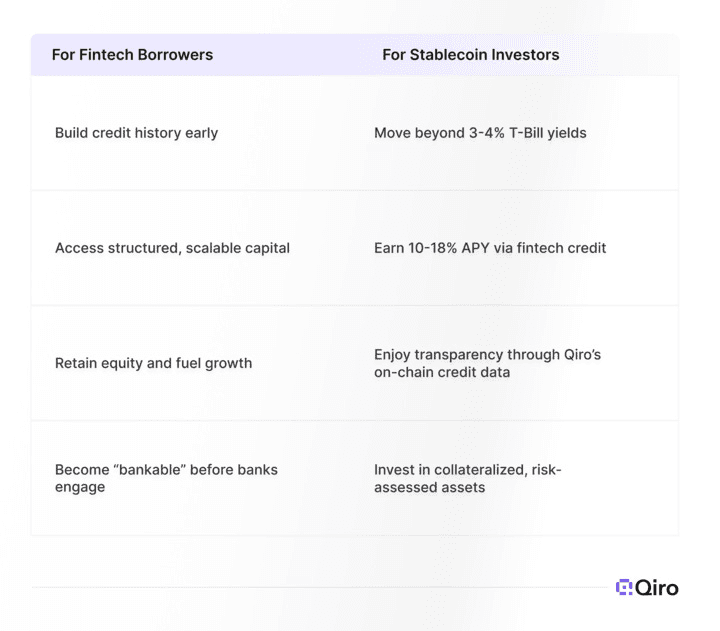

Why you should care

Stablecoin investors can now access 10-18% APY yields - not from looping, but from real, short-duration fintech receivables.

Borrowers get faster access to capital without waiting years for bank approvals.

Every loan passes through Qiro’s independent underwriting system, filtering out weak borrowers and reducing default risk.

The infrastructure flywheel

Qiro isn’t just another marketplace - it’s an underwriting layer any liquidity provider, marketplace, or protocol can plug into.

This reusable credit brain:

Standardizes fintech underwriting,

Reduces time and cost of due diligence,

Enhances transparency for lenders, and

Creates a pipeline of reliable, verified credit assets.

This is how global credit becomes scalable.

Why it works for both sides

The next era of credit is hybrid - combining:

On-chain transparency + Off-chain diligence

Stablecoin liquidity + Institutional discipline

Global reach + Local compliance

And Qiro Finance is the bridge - powering the infrastructure, credit evaluation, and risk management that make it all work.

The takeaway

Fintech founders who start borrowing early don’t just raise money - they raise credibility.

Stablecoin investors who start lending early don’t just chase yield - they access the next trillion-dollar asset class.

Because cash builds comfort.

Debt builds velocity.

And infrastructure builds trust.

Get in touch

If you’re an on-chain / Web3 fintech (cross-border payment, remittance, stablecoin payments, stablecoin-backed card issuer, etc) or a digital fintech (invoice financing, factoring, BNPL, or trade finance) looking to borrow capital, let’s talk.

If you’re sitting on idle stablecoin capital or treasury, or a stablecoin investor seeking double-digit yields without looping or leverage, reach out.

Qiro takes care of risk evaluation, yield structuring, and credit history building - so you can focus on scaling or earning.

Email: akshay@qiro.fi

Telegram: @akki_vaga