Qiro Weekly Newsletter - Vol. 1

Share Now:

Welcome to the pilot edition of our newsletter.

Each week, we’ll share perspective-driven takes in the evolving crypto and fintech landscape, blending market insight, original thinking, and research-backed observations. Our goal isn’t to chase headlines, but to distill what truly matters, why it matters, and where things are headed next.

Thanks for reading Qiro Finance ! Subscribe for free to receive new posts and support my work.

deStablecoin Season

This week might go down as one of DeFi’s most revealing chapters yet, not because of a hack or exploit, but because of how capital was recycled across protocols in ways few understood until it was too late. This is the story of xUSD (Stream Finance), deUSD (Elixir Network), and the recursive minting loop that took down what many believed were “institutional-grade” stablecoin yield systems.

For months, both Stream Finance and Elixir Network marketed themselves as the next evolution of on-chain stability.

Stream Finance issued xUSD, a so-called yield-bearing stablecoin backed by “market-neutral” trading strategies.

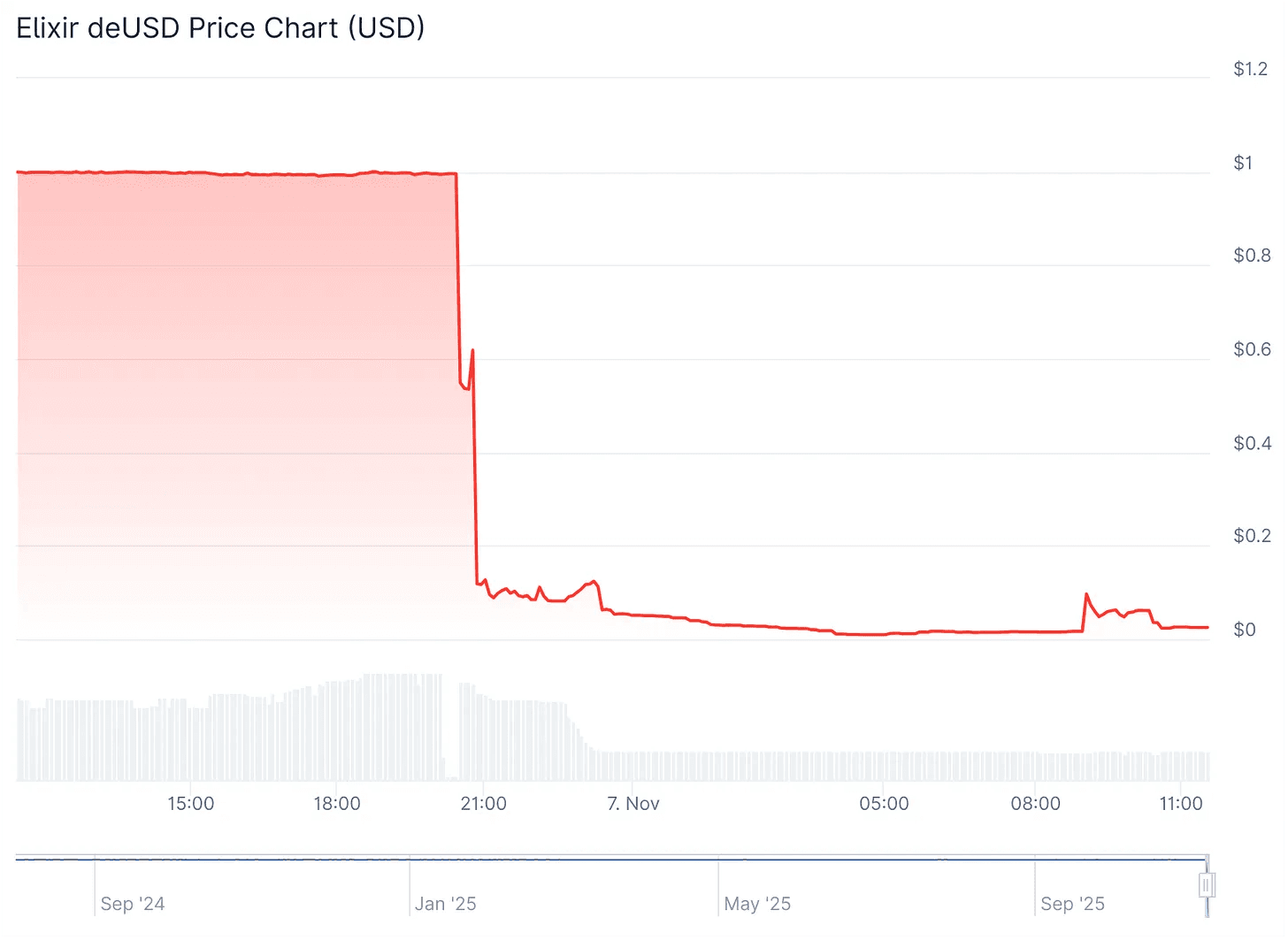

Elixir Network issued deUSD, claiming to be a stablecoin backed by real-world assets like U.S. Treasuries and staking yields.

Both promised transparency and institutional credibility — the kind of language that reassures users and attracts big liquidity. But beneath that facade, both protocols were quietly leveraging each other’s tokens to create yield from thin air.

The Recursive Loop (Explained Simply)

On October 28, on-chain researchers @Schlagonia began tracing funds flows from xUSD that looked too clean, and too circular to be organic.

Here’s how the recursive loop worked:

1. Users deposited USDC into Stream Finance to mint xUSD.

2. Stream sent that USDC on another chain, swapped for USDT, and used it to mint deUSD on Elixir.

3. The freshly minted deUSD went back into Stream’s ecosystem as collateral to borrow more USDC.

4. That borrowed USDC was then used to mint more xUSD.

The cycle repeated — again and again.

In effect, the same USDC collateral was reused multiple times to issue overlapping claims on value. What looked like $500M+ in assets on paper may have represented less than a fraction of that in real backing. It wasn’t yield; it was leverage masquerading as innovation.

The Warnings Start

As charts and wallet traces circulated on Crypto Twitter, warnings grew louder and louder.

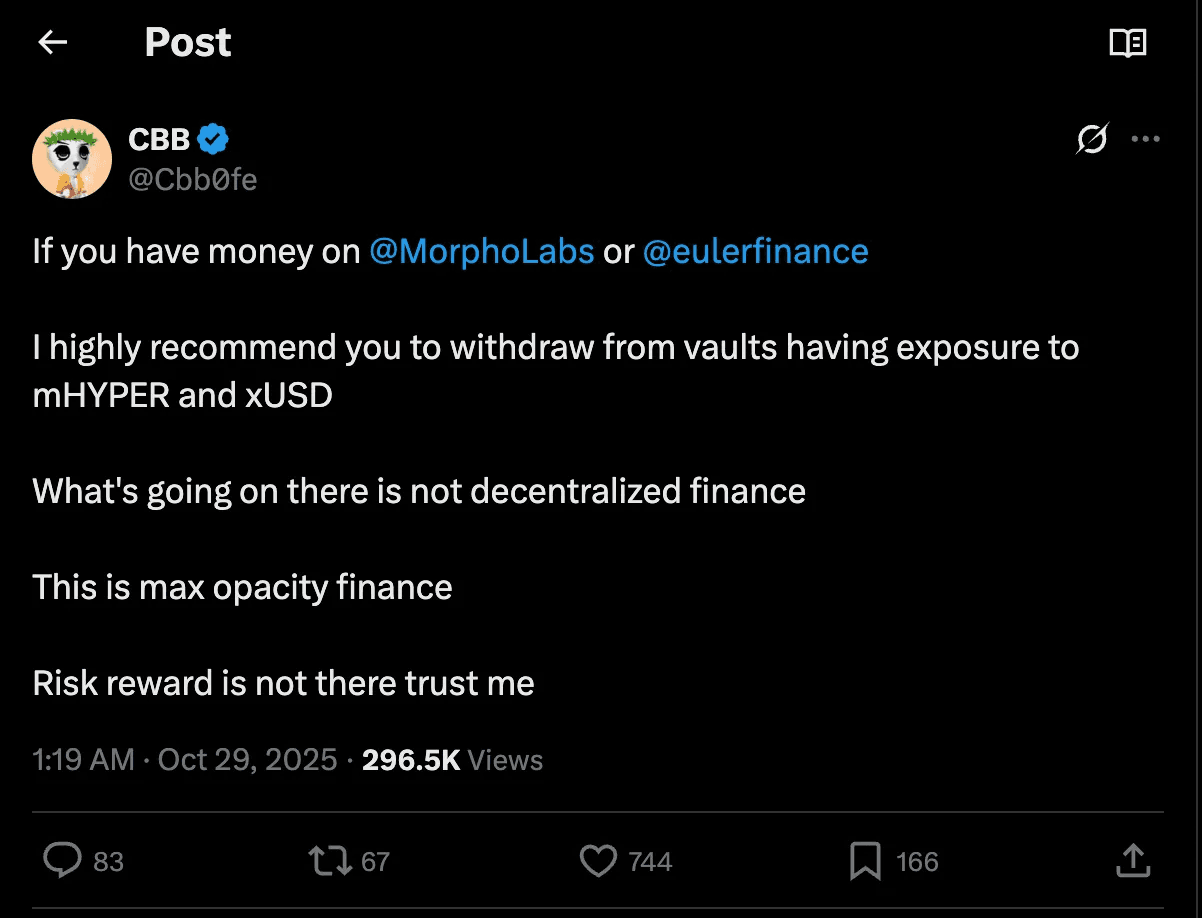

On October 29, DeFi researcher/KOL @Cbb0fe posted a warning to users for withdrawal on the vaults related to mHYPER and xUSD.

Liquidity providers started to notice something was off:

Everyone started asking xUSD team to publish proof of reserves, which was never published.

deUSD was showing suspiciously low volume relative to its claimed backing.

Inverse Finance delisted the markets for deUSD

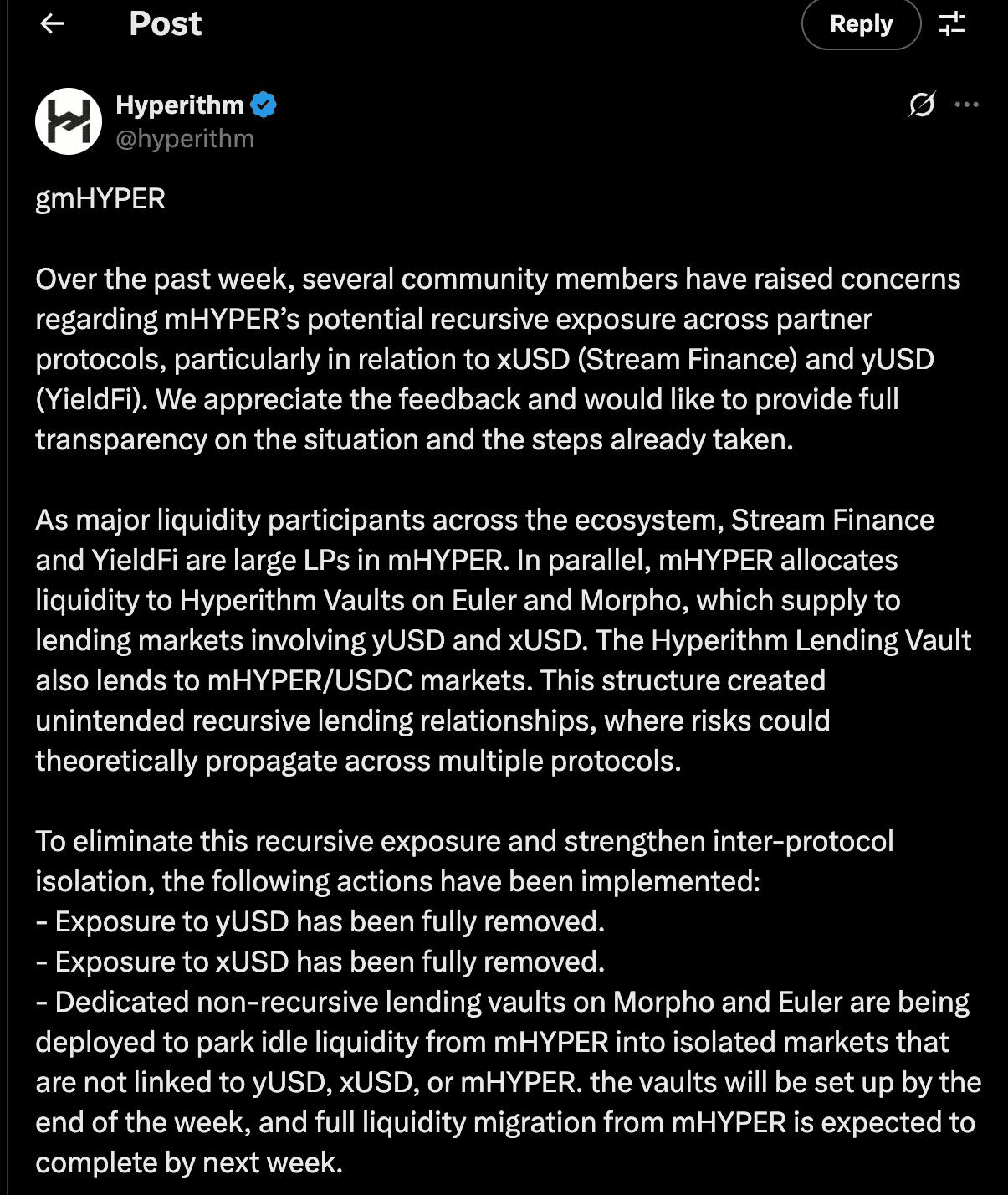

As people started raising concerns on The mHYPER vaults (Hyperithm’s liquidity aggregator) which were exposed to both xUSD and yUSD markets. As the response, The yield manager, Hyperithm took action and pulled the entire $10 million out before all this went bust.

The Collapse

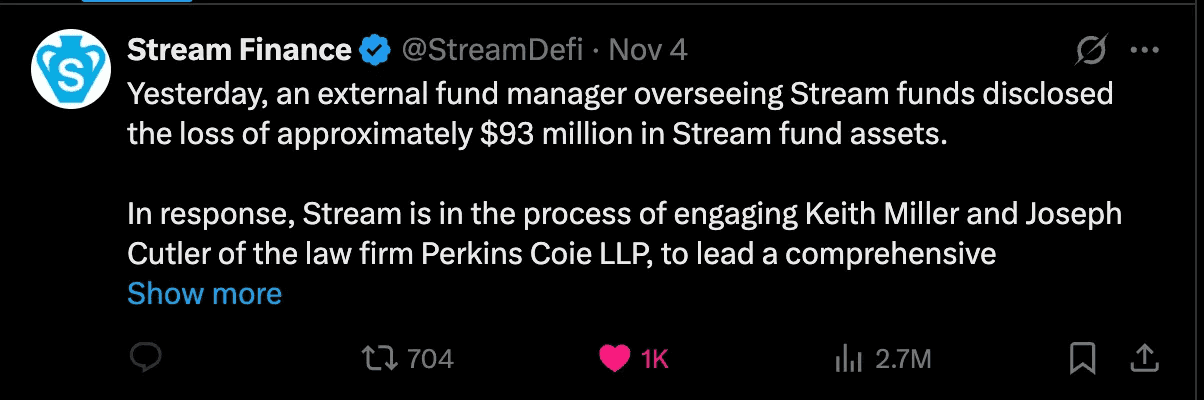

Then came November 4.

Stream Finance disclosed a loss of approximately $93 million, citing an “external fund manager” who had “failed to report trading losses.”

Translation: a large chunk of the supposed backing for xUSD simply didn’t exist anymore.

Within hours, xUSD depegged — crashing from $1.00 to as low as $0.16. Liquidity dried up instantly. Vaults froze. Arbitrage vanished.

Then came the barrage of tweets, with Elixir claiming senior 1-1 rights as they unwound their position with Stream. After which Elixir’s deUSD depegged and hit rock bottom, and an hour ago they announced a shutdown of the whole project.

And because Elixir’s deUSD was heavily used within Stream’s system, it quickly followed. The loop reversed itself: as xUSD collapsed, the collateral for deUSD evaporated. leading to a chain reaction across lending protocols that held exposure to both.

By the end of the weekend:

xUSD was effectively worthless.

deUSD had depegged and Elixir announced its shutdown.

mHYPER, a major allocator, confirmed that all exposure to xUSD and yUSD had been removed and new isolated vaults were being deployed to prevent recursion.

Where is the yield coming from?

The main question ended up being, is there a future fix? Such an event is always avoidable, you must always understand risk, and the source of the yield.

Monolithic vs Modular lending markets

This market event triggered a heated online between certain Aave & Morpho representatives about Monolithic and Modular design in the lending protocols.

Aave being a monolithic lending protocol all markets share liquidity are governed by the Aave DAO, which had 0 exposure to any of the assets which went bust. On the contrary in modular protocols like Morpho and Euler, risk curators would manage isolated vaults, this enables lending markets with diverse set of collateral.

A lot of liquidity providers trusted the curators on these protocols to curate risk. But many of them had stablecoin lending markets against these risky assets which eventually went bust. The actions of a few curators led to a systemic crisis putting multiple funds’ and users’ liquidity at risk.

The monolithic approach is simple but restrictive as it shares liquidity and hence cannot allow much flexibility. Modular approach helps users select risk profiles and introduces curator driven risk management. But it comes with higher complexity.

Aave has allowed new and upcoming looping strategies to begin crowding our lower risk overcollateralized lending activity, moving forward the market will have a sharper eye on the risk-adjusted returns too, solving issues like Aave v3 markets are not perfect for margining long tail assets and tokenized hedge funds.

In the end, diversity of curators and lending infrastructure is necessary as long as we don’t foster unhealthy ‘yield-chasing from curators’ and focus on better transparency and visibility into protocol and curator risk, to allow users to make informed decisions with their money.

Which one of the two lending approaches is better is for the market to decide, as DeFi lending grows from here.

Closing Thoughts

For all the sophistication and “institutional structure” promised, the past week was a reminder that leverage and opacity remain DeFi’s biggest systemic risks. The industry needs better underwriting and transparent risk management at its core.

At Qiro, we’re building a transparent underwriting framework designed to eliminate adverse selection and surface only the highest-quality private credit opportunities protecting investors above all else.

P.S. Interested in earning 12–15% fixed APY through tokenized private credit opportunities? You’re in the right place.

Qiro Early Access Form

Until next week 🫡