Inside mGLOBAL: Tokenized Exposure to Fasanara's GDADF

Share Now:

Inside mGLOBAL: the full 38-page report. Read it here

Executive Summary

This report provides insights into the structure, mechanics, and key considerations of the mGLOBAL token, a tokenised investment note issued by the Aureum Securitisation Compartment under Luxembourg securitisation law, which provides investors with indirect exposure to the GDADF private credit strategy. Unlike direct investors in the GDADF, mGLOBAL holders do not own fund shares and instead hold a claim against the issuing compartment. The compartment allocates approximately 90% of assets to GDADF shares while maintaining up to 10% in stablecoins to facilitate on-chain liquidity management and redemption functionality.

Accordingly, the investment should be viewed as a multi-layered structure combining traditional private credit exposure with securitisation, tokenisation, and digital asset infrastructure. Each intermediary layer serves a dual function: it introduces its own legal, operational, and technological considerations, but also provides distinct protections including legal segregation, bankruptcy remoteness, compartment ring-fencing, on-chain transferability, and defined liquidity functionality. Investors should assess both the performance and credit quality of the underlying GDADF portfolio and the structural trade-offs arising from these intermediary layers.

mGLOBAL’s direct collateral exposure is to GDADF (total AUM: USD 1.14bn), the fund covered in this report. Per Fasanara, GDADF sits within a broader USD 3.5bn ABF / receivables platform, reflecting the wider scale and institutional infrastructure supporting the strategy. The GDADF portfolio comprises 700,000+ open positions across 60+ countries with a 60-90-day average duration, and has delivered a gross 9.01% CAGR since September 2017 with zero negative monthly returns a track record maintained through COVID-19, Greensill, FTX/TerraLuna, and the First Brands episode. The analysis covers the underlying private credit assets and fund structure; the Aureum securitisation vehicle and associated legal framework; stablecoin and liquidity management arrangements; custody and operational dependencies; smart contract and blockchain infrastructure considerations; redemption mechanics; counterparty exposures; and regulatory landscape.

The objective is to equip investors and protocols with the structural understanding needed to evaluate how mGLOBAL delivers economic exposure to GDADF, and the trade-offs involved in exchange for tokenised accessibility, transferability, and liquidity. For investors seeking formal underwriting or risk parameter setting for on-chain deployment, Qiro Finance offers dedicated credit curation services.

Section 1 - mGLOBAL Token Overview

mGLOBAL provides tokenised exposure to a granular portfolio of short-dated, self-liquidating SME trade receivables and invoices, with average obligor quality in the A/BBB range and repayment driven by diversified corporate obligors. This is not generic long-duration private credit: the 60-90-day average portfolio duration means the book self-liquidates within 2-3 quarters through natural run-off, providing an inherent liquidity backstop.

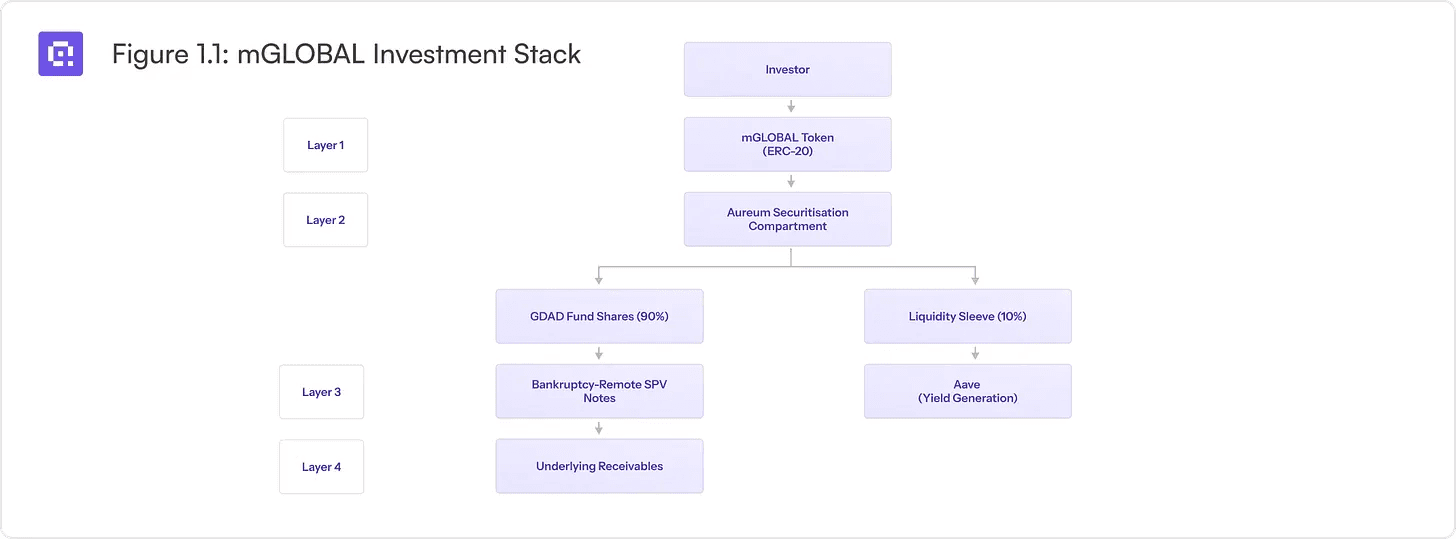

In addition to the traditional (TradFi) fund subscription route, investors can gain exposure to the GDADF strategy through mGLOBAL, a tokenised note issued under Luxembourg law. mGLOBAL provides on-chain access to the same underlying portfolio with enhanced liquidity options, while introducing a distinct legal wrapper with its own protections and trade-offs.

The Issuer invests approximately 90% of note proceeds into shares/units of the GDADF, with up to 10% of Compartment NAV held in cash, USDC, or other permitted stablecoins for liquidity and operational purposes, including instant redemptions. The 10% instant liquidity sleeve is deposited in approved DeFi lending markets (currently Aave) to generate yield while remaining available for atomic redemption. The 10% instant sleeve is only one layer of a multi-tier liquidity waterfall. L2 Midas Staked Liquidity (USD 20M) and the L3 OTC facility (USD 100M Fasanara affiliates + USD 30M InfiniFi) are separate, independently funded redemption pathways. In addition, the Standard monthly redemption route (35 days) provides a full-capacity exit option for all holders.

Figure 1.1: mGLOBAL Investment Stack

1.1. Instant Liquidity Sleeve (10%)

The 10% instant liquidity sleeve is currently deposited in approved DeFi lending markets (currently Aave) to generate yield, though the mandate permits allocation to other highly liquid instruments including Treasury bills, tokenised Treasury products, and money market exposures. The purpose of this allocation is to facilitate subscriptions, redemptions, and day-to-day liquidity management without requiring immediate liquidation of the underlying GDADF position.

From an investor perspective, the liquidity sleeve serves as a liquidity transformation mechanism, helping bridge the mismatch between the relatively illiquid nature of private credit investments and the liquidity expectations of tokenised financial products. While this structure enhances redemption flexibility and operational efficiency, it also means investors do not receive full exposure to the GDADF portfolio at all times. Portfolio performance may therefore differ modestly from that of a direct GDADF investment, depending on the relative returns generated by the liquidity sleeve and the underlying credit assets.

The potential for cash drag during the subscription deployment window is mitigated by the Aave sleeve, which earns yield on idle capital rather than leaving it unproductive. Importantly, only the 7% holdback amount is subject to this interim treatment - not the full subscription - so the actual yield impact from deployment latency is marginal.

1.2. GDADF Shares (90%)

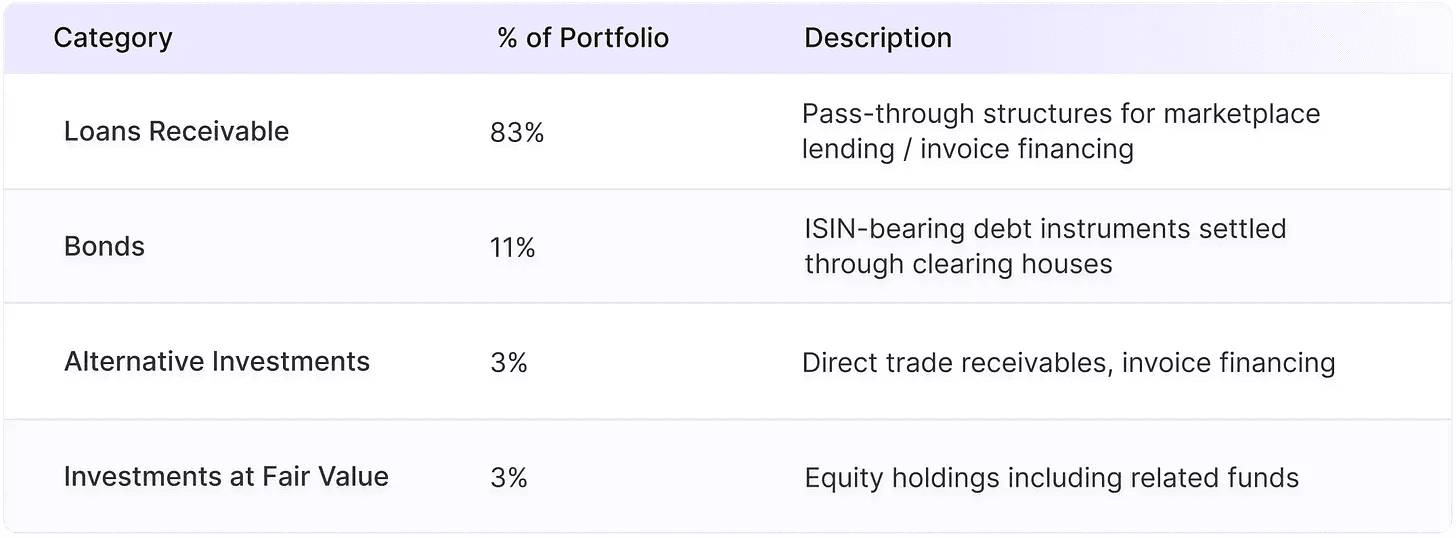

The 90% GDADF allocation is deployed across four asset categories: SME Trade Receivables (83% of portfolio, 60-90-day average maturity), Bonds (11%, ISIN-bearing instruments settled through clearing houses), Alternative Investments (3%, direct receivables and invoice financing), and Fair Value holdings (3%, equity holdings including related funds). This allocation mirrors the GDADF’s own portfolio composition.

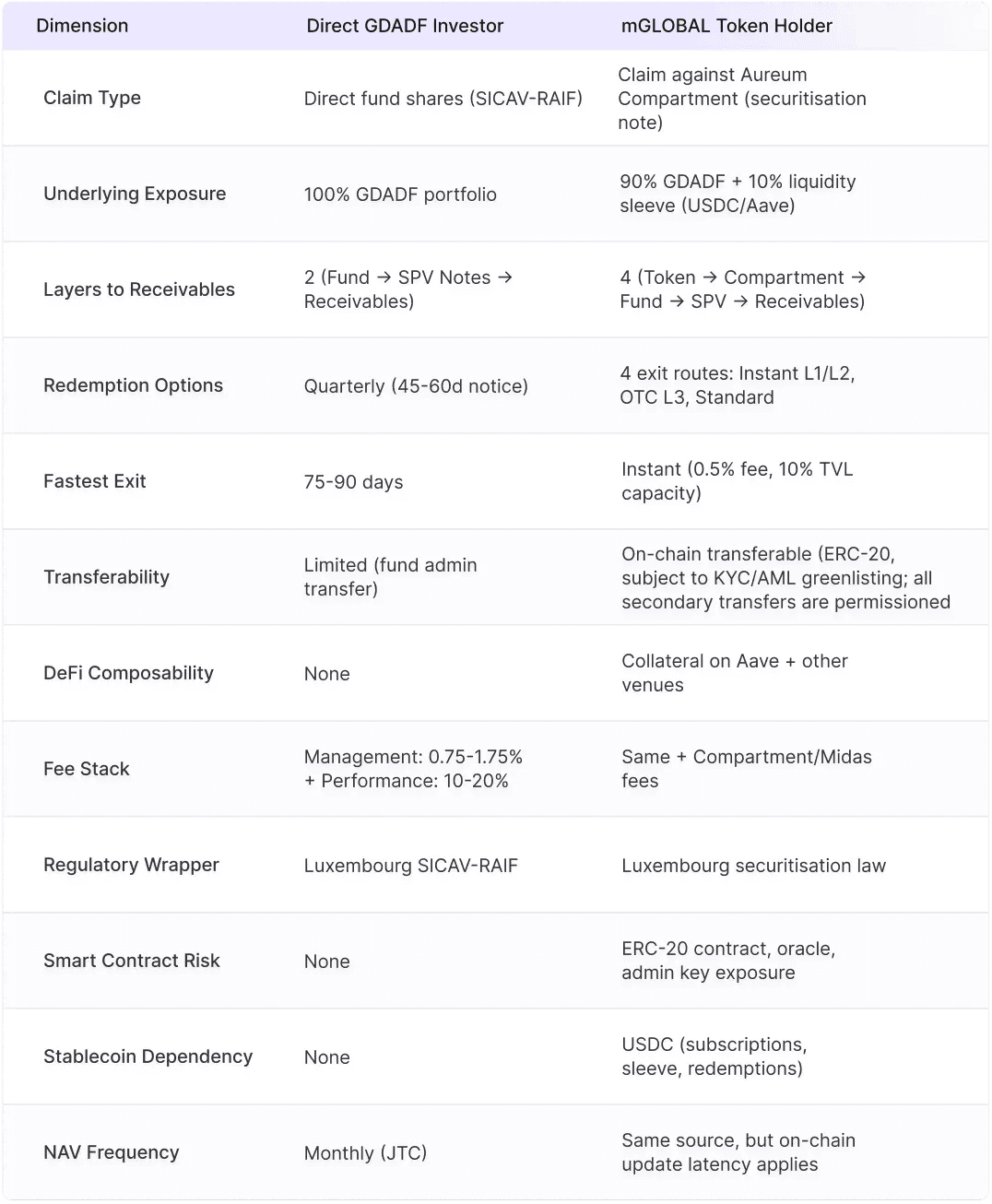

Table 1.1: Direct GDADF vs mGLOBAL comparison

Qiro Lens: The comparison above captures the core structural trade-off. The mGLOBAL wrapper introduces additional token-layer considerations (smart contract, stablecoin, platform, oracle), but these also serve as access and protection layers. The structure adds instant redemption, on-chain transferability, DeFi composability, Luxembourg securitisation ring-fencing, and compartment-level creditor recourse. Whether the trade-off nets positive depends on the allocator’s liquidity profile and infrastructure comfort.

Section 2 - mGLOBAL Underlying: GDADF

The Fasanara Capital Global Diversified Alternative Debt Fund (GDADF) is a Luxembourg SICAV-RAIF providing institutional investors with exposure to a granular portfolio of ultra short-dated trade receivables, digital invoices, and SME-originated loans. The fund operates a multi-platform, structured pass-through model: Fasanara does not lend directly 141 approved fintech originators source receivables that are sold to bankruptcy-remote SPVs under Fasanara’s control, which issue senior notes purchased by the fund.

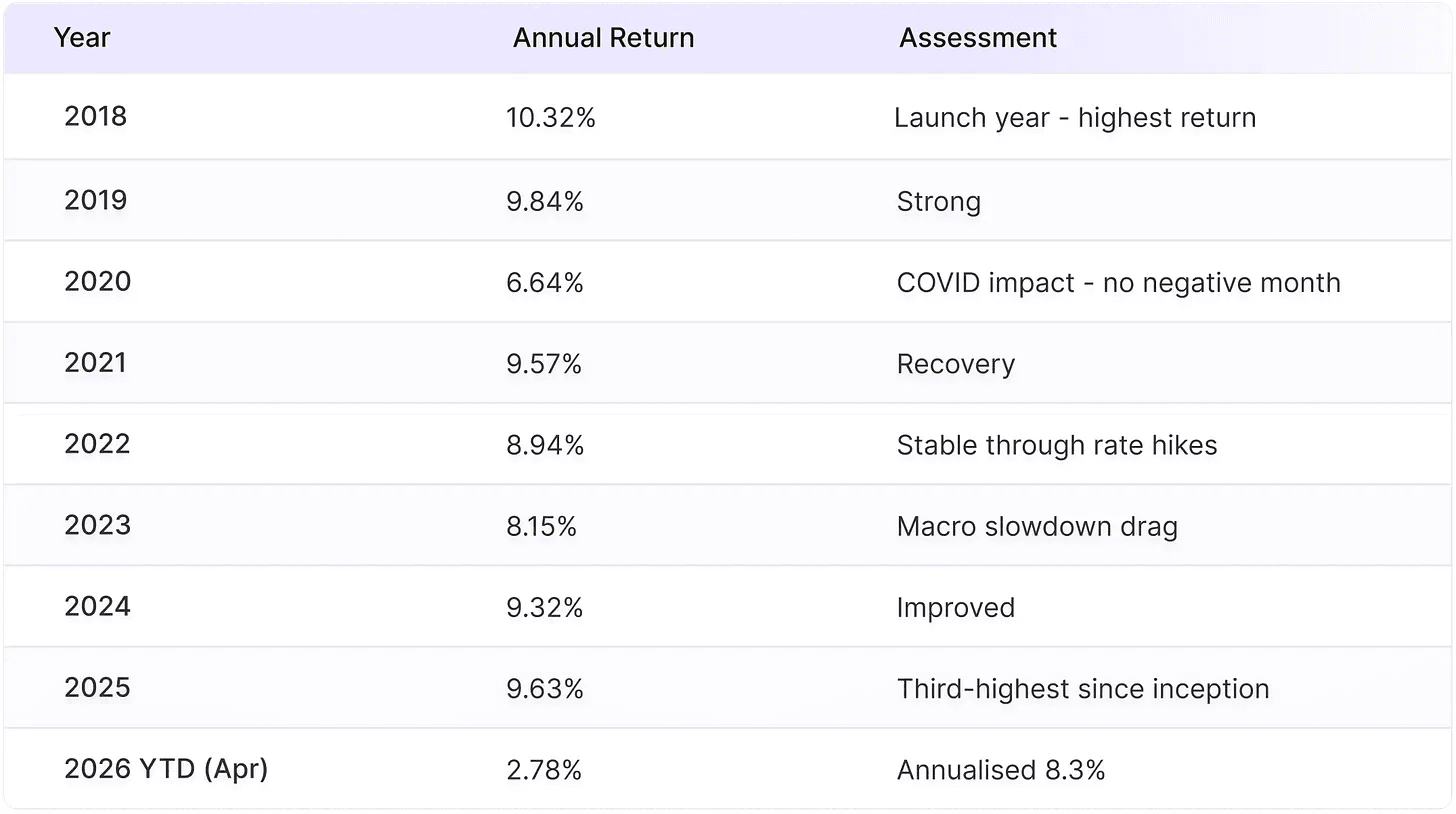

As of April 2026, GDADF AUM stood at USD 1.14Bn across 73 active originators. Per Fasanara, the fund sits within a broader USD 3.5Bn ABF / receivables platform across multiple vehicles, across 60+ countries, 10+ sectors, and over 700,000 open positions. The fund targets net 6-8% p.a. in EUR (8-10% in USD) with low volatility, and has delivered a gross 9.01% CAGR since inception with no negative monthly return across multiple stress events including COVID-19, Greensill, FTX/TerraLuna, and the First Brands collapse.

2.1. Fund Facts

Table 2.1: Fund Facts

The a(f) rating by ARC Ratings (an ESMA-registered Credit Rating Agency) is an independent assessment of the fund’s exposure to factors that could lead to unexpected NAV and total return volatility. The “a” level indicates strong ability to preserve NAV with low sensitivity to adverse conditions. ARC’s methodology evaluates portfolio quality, diversification, liquidity management, leverage, and operational infrastructure.

2.2. Key Portfolio Metrics

Table 2.2: Key Portfolio Metrics

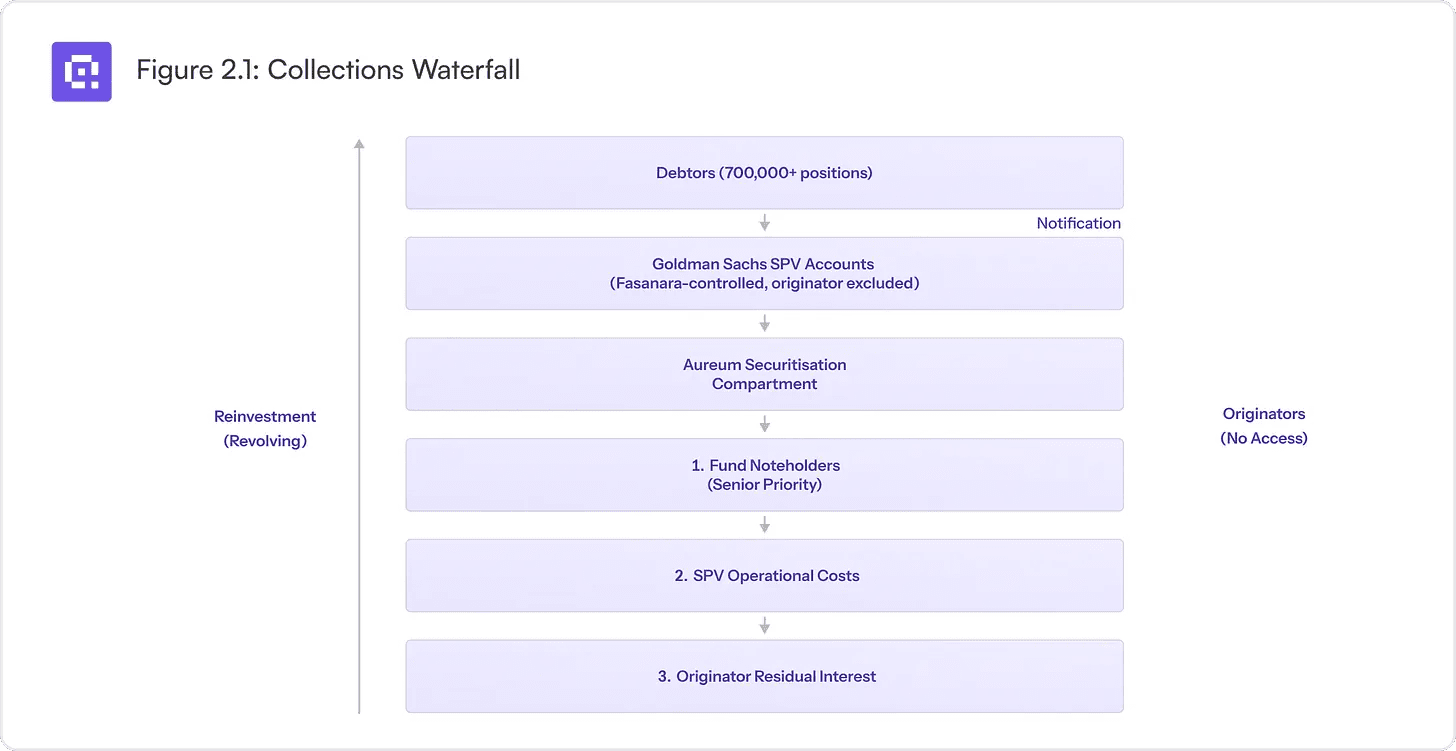

Key Structural Feature: The fund’s credit protection operates through bankruptcy-remote SPVs with originator first-loss provisions of 5-30%, credit insurance via Allianz Trade/Euler Hermes, and an average senior tranche attachment point of 17.1%. Collections flow directly from debtors into Fasanara-controlled Goldman Sachs accounts originators have no access to collection accounts. The payment waterfall prioritises fund noteholders first.

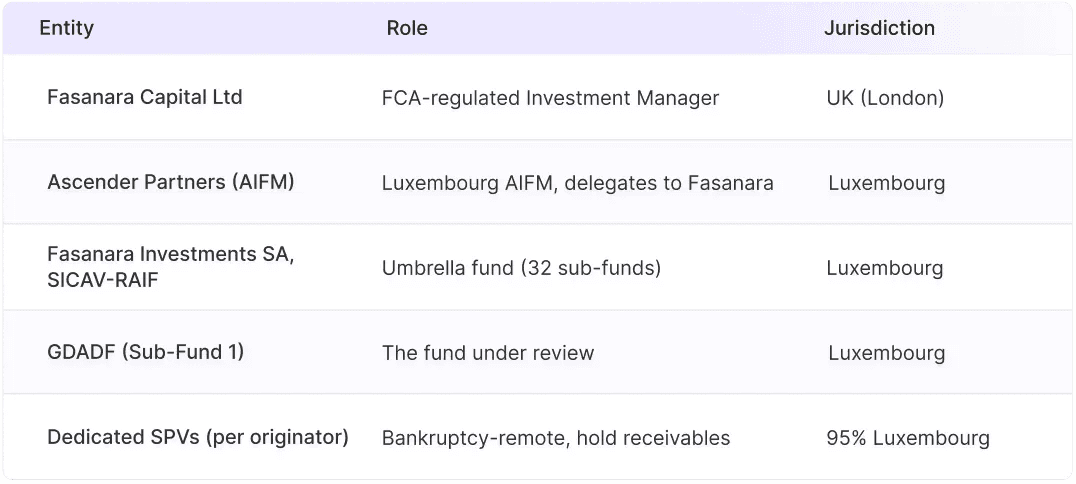

2.3. Fasanara Capital - Group Overview

Fasanara Capital Ltd, founded in 2011, is fully authorised and regulated by the UK Financial Conduct Authority (FCA). The firm manages USD 6Bn AUM (April ‘26) in fintech strategies on behalf of pension funds and insurance companies in Europe and North America. With 130 employees across London (HQ), Abu Dhabi, Amsterdam, and offices opening in Italy (September 2026) and New York (June 2026), Fasanara is the largest and longest-standing fintech lending fund manager in Europe.

Powered by its proprietary technology platform with 141 fintech lenders integrated from over 60 countries, Fasanara has arranged cumulative lending of USD 115Bn. The technology was spun off into a separate entity in which Blackstone acquired a 20% minority stake, now using the platform for approximately USD 80Bn of Blackstone’s private credit AUM - validating the institutional quality of the technology stack.

Table 2.3: Entity/Jurisdiction

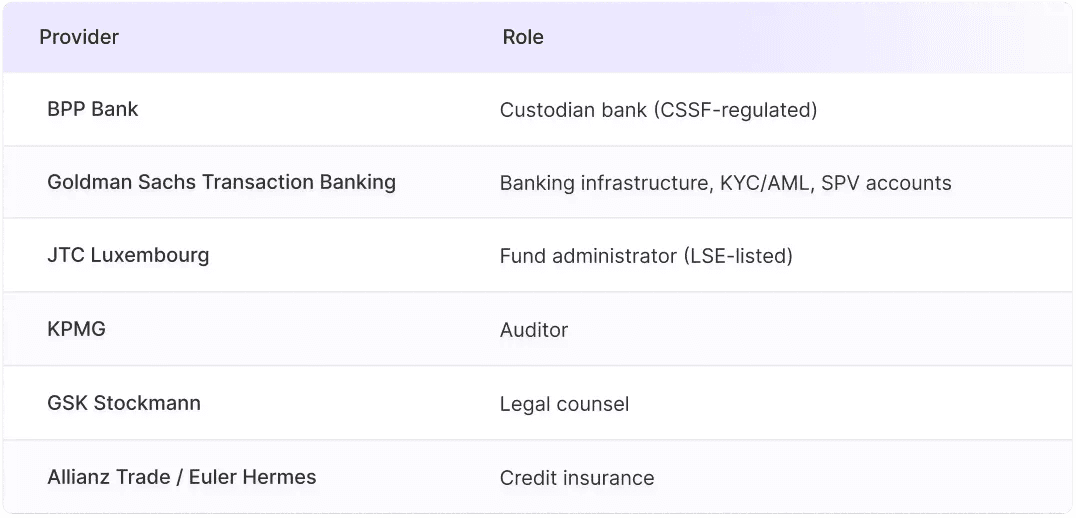

2.4. Key Service Providers

Table 2.4: Key Service Providers

2.5. Governance & Management

Board of Directors: 3 members (2 independent, 1 Fasanara employee) - lean structure for a USD 6Bn firm. Key management: Francesco Filia (Founder & CEO, 20+ years, ex-BofA Merrill Lynch), Elisa Bianchi (CCO, ex-Merrill Lynch/Credit Suisse), Francesco Vaccari (COO, ex-Deutsche Bank AM), Matteo Amaretti (Managing Partner).

The Board and KMP are supported by Investment, Risk Management, Senior Managers, and Valuation Committees. Advisory Board comprises 12 members including representation from APG Asset Management (2 members), CDPQ (2 members), and Generali Insurance - strong institutional backing.

2.6. GDADF Investor Profile

134 investors; 90% institutional (pension funds, insurance companies, banks, supranational institutions), 10% family offices/HNWIs. No single investor exceeds 10% of AUM. Dutch and Italian investors account for 60% of the GDADF investor base. Top 10 investors hold 39% of AUM cumulatively.

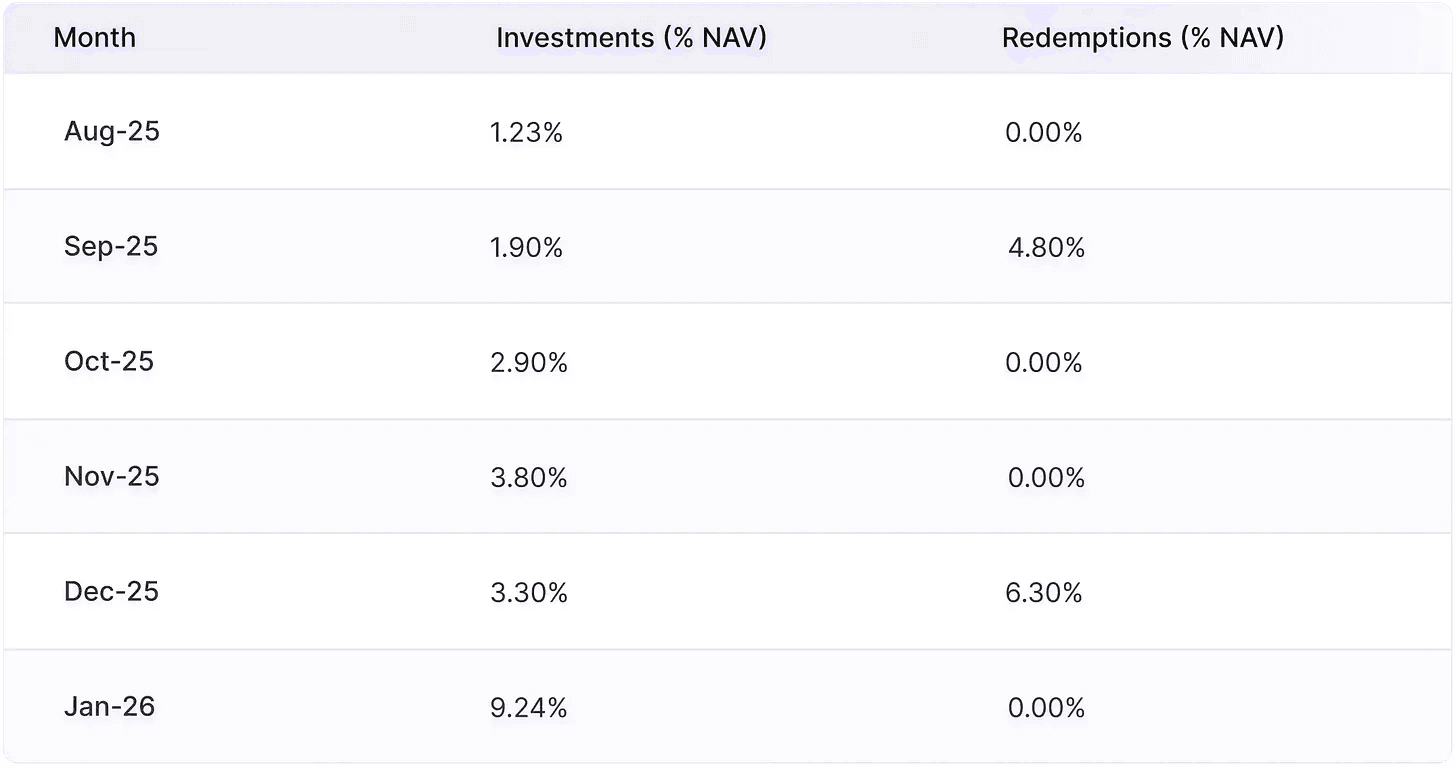

Table 2.5: Investor Flows

This shows net positive flows in 5 of 6 months. The January 2026 inflow of 9.24% of NAV is the largest single-month subscription in recent history, suggesting strong ongoing institutional demand. Investor type breakdown (last 6 months of new investments): Dutch Family Office 29%, Italian Pension Fund 24%, UK Insurance 10%, Italian Bank 10%, Italian Family Office 7%, Belgian Pension Plan 2%, European Private Bank 2%, Other 16%. This confirms the fund’s European institutional bias and the dominance of pension/insurance capital which tends to be sticky and long-duration.

2.7. GDADF Product & Strategy

GDADF is an open-ended fund targeting stable net returns of 6-8% p.a. in EUR (8-10% in USD) with low volatility. Fasanara does not lend directly. Originators source loans/receivables that are sold to bankruptcy-remote SPVs under Fasanara’s control. These SPVs issue senior and junior notes; the fund invests at the senior level.

Table 2.6: Portfolio Composition

The fund secures an otherwise unsecured lending sector through four pillars: seniority (no leverage, no subordination), recourse (first-loss provisions 5-30%, credit insurance, government/corporate guarantees), over-collateralisation (advance rates <90%), and diversification (60+ countries, 141 originators, 700,000+ positions). Approximately 75% of GDADF AUM is covered by at least one form of credit enhancement, with first-loss buffers, insurance, the 17.1% average senior attachment point, controlled collections, and the senior-first waterfall directly reducing expected loss.

Approximately 25% of exposures are not covered by first-loss, credit insurance, or guarantees - by design. These positions typically involve investment-grade obligors (average rating A/BBB, in line with the fund-level average) where adding layered credit enhancement would be redundant and cost-inefficient. Importantly, these exposures still benefit from structural over-collateralisation through the fund’s 70-90% (85% average) advance rate on face value, meaning Fasanara holds a built-in equity cushion even where explicit credit wraps are absent. The average attachment point for senior tranches is currently 17.1%.

2.8. Fund Structure & Economics

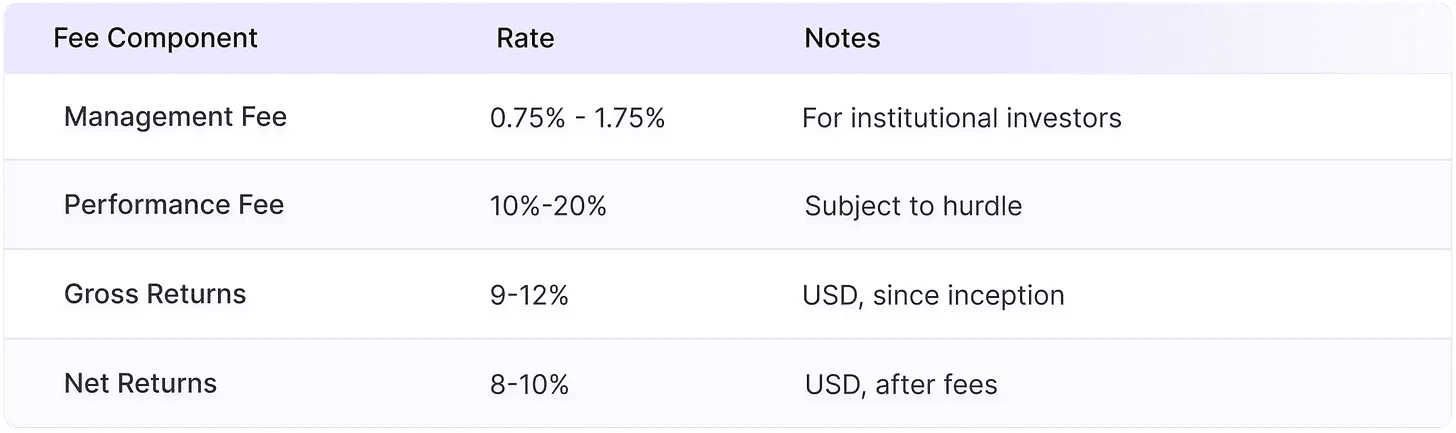

The fund operates with an all-equity capital structure and no leverage. Leverage ratios of 111% (Gross) and 118% (Commitment) sit well within the 300% regulatory limit. Gross returns of 9-12% in USD are achieved purely through asset yields, translating to 8-10% net returns.

Table 2.7: Fee Structure

Collections on underlying receivables flow directly from debtors into segregated SPV bank accounts within Fasanara’s Goldman Sachs Transaction Banking environment. Originators have no access to or control over these accounts. Each SPV adheres to a predefined payment waterfall: collections are applied first to noteholders, then to SPV operational costs, and finally any residual interest to the originating platform.

Figure 2.1: Collections Waterfall

2.9. Financial Performance

Table 2.8: Fund Returns (Gross Annual USD)

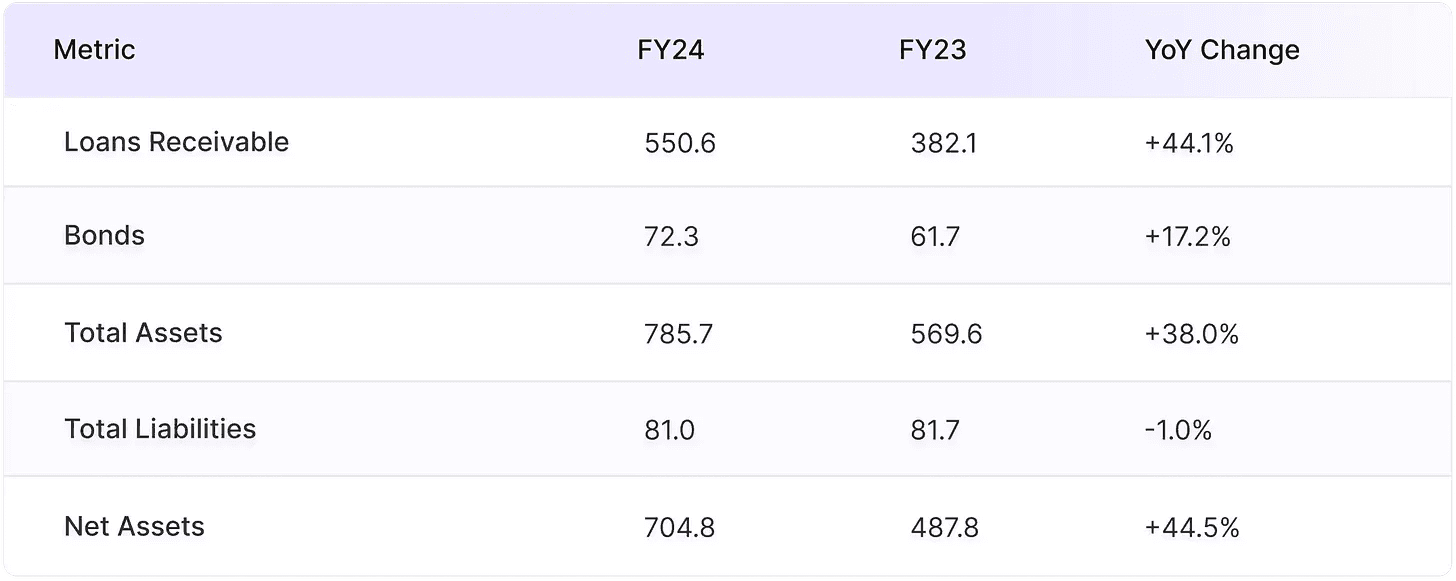

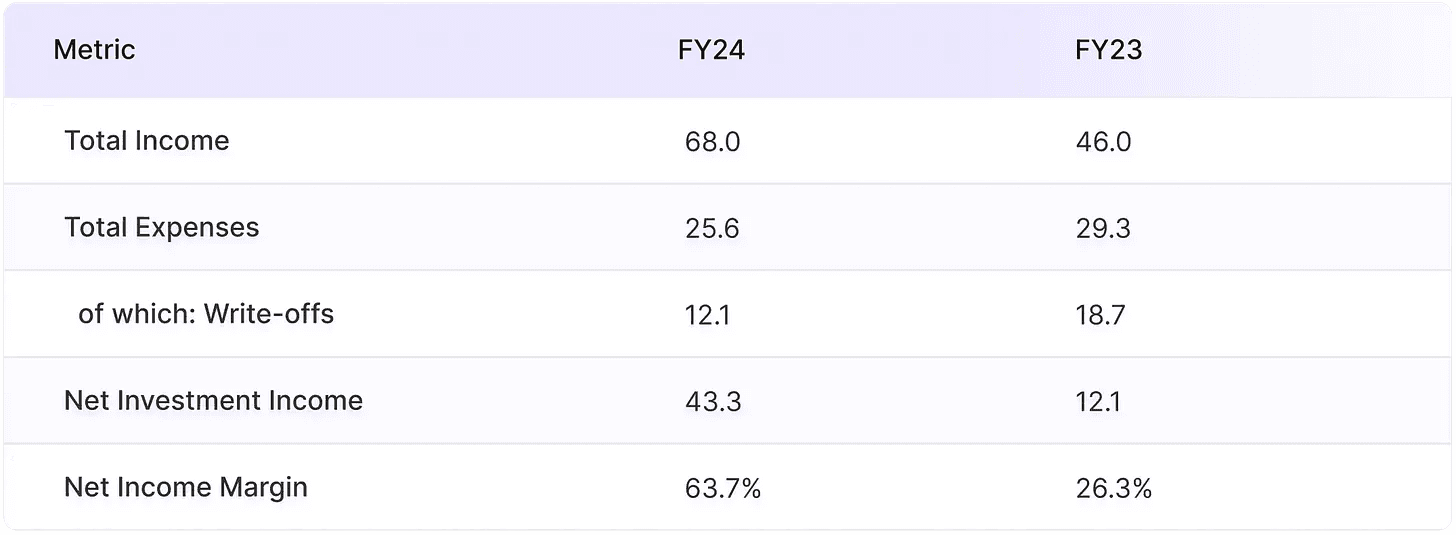

Table 2.9: Statement of Net Assets (EUR, Mn)

Table 2.10: Key P&L Metrics (EUR, Mn)

Income is driven by loans receivable (83.8% of total income in FY24). Write-offs fell 35.3% but remain the largest expense line. FX hedging consumed EUR 12.96M in direct costs (19% of gross income). The fund ended FY24 with 44.5% growth in net assets, materially influenced by the Sub-Fund 14 merger contributing EUR 165.6M.

2.10. Underwriting & Risk Management

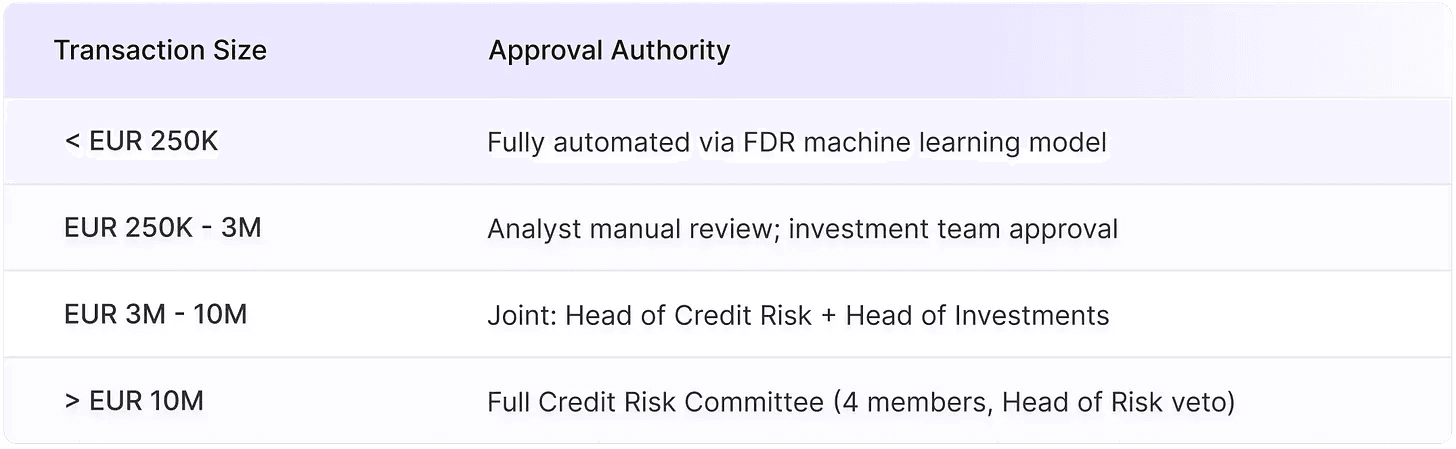

The fund operates an open-architecture model with 141 approved fintech partners selected from a universe of 1,300 originators (11% approval rate). Each originator relationship is Risk Committee-approved and continuously monitored through Fasanara’s technology-enabled systems. Full due diligence was conducted on 465 originators, with 324 rejected or pending. A 14-step due diligence process includes standardised templates, full loan tape rebuilds, 2-3-day on-site visits, and Risk Committee approval (Head of Risk holds veto power).

Table 2.11: Transaction Approval Authority

Fund Level: PPM limits, internal risk guidelines, HHI index (currently 8 bps, equivalent to 12,500 equally-weighted positions), concentration limits, credit VaR as master risk indicator.

Originator Level: Ongoing monitoring, annual credit reviews, originator/platform ratings incorporating KPIs.

Single Trade Level: Automated eligibility rules, FDR scoring, fraud checks, real-time asset tracking.

2.11. Structural Protections

Each originator relationship operates through a dedicated SPV owned by an orphan Dutch foundation (stichting) with no legal connection to originator or arranger. Receivables are transferred via true sale, and the fund holds direct creditor rights against debtors through Notice of Assignment. Under Luxembourg RAIF law, each sub-fund’s assets and liabilities are legally ring-fenced from those of other sub-funds within the same umbrella.

SPV structures incorporate eligibility criteria, concentration limits, financial covenants (cash runway, EBITDA, LTV, max 90% advance rate), trigger covenants (DPD 30+/60+ thresholds, default rate triggers, stop-funding mechanisms), and reporting undertakings.

Valuation is not marked-to-model; it is marked-to-market based on observable days of delay. Monthly NAVs produced by JTC Luxembourg, approved by AIFM valuation committee, with Fasanara internal review and annual KPMG audit. This multi-layered valuation governance ensures that token pricing is anchored in formal fund valuation processes rather than discretionary token-level pricing. KPMG has issued an unqualified audit opinion on the GDADF financial statements for FY24 and all prior years since inception.

2.12. GDADF Key Considerations

Credit & Default Trajectory: The annualised default rate rose from 0.5% (2022) to 0.9% (2023), 1.0% (2024), and 1.17% (2025). Crystallised losses stood at 0.40% for FY25. Historical annual default rates: 2018 (0.3%), 2019 (0.4%), 2020 (2.19% - COVID peak), 2021 (0.6%), 2022 (0.5%), 2023 (0.9%), 2024 (1.0%), 2025 (1.17%). Crystallised losses have remained below 1% every year. The First Brands exposure - a UK-based consumer goods company that entered administration in 2024 - was contained at 0.10% of NAV. First-loss buffers have been breached at least 20 times historically, but the fund has never posted a negative month. This trajectory is consistent with the broader European SME credit cycle, where defaults have climbed post-COVID and now appear to be approaching cyclical peaks. The level of defaults observed remains within the fund’s structural absorption capacity, supported by credit enhancement layers and the short 60-90 day portfolio duration.

Table 2.12: Concentration Limits

Concentration: UK (22%) and US (16%) together account for 38% of NAV. Currency exposure concentrated in EUR (70%) and GBP (16%). The top two originators each hold 14% of the book.

Structural Protection Design: Approximately 25% of GDADF exposures do not benefit from first-loss protection, credit insurance, or government/corporate guarantees. (see Section 2.7 for design rationale)

Illiquidity of Notes: The Board may suspend redemption of shares if there are significant redemptions. The 12.5% quarterly NAV gate means amounts exceeding the gate roll over to the next quarter.

Originator Risk: Approximately 20 originators have been discontinued since inception. Backup servicer arrangements are always in place, with status ranging from ‘cold’ to ‘hot/warm’.

FX Hedging Drag: FX hedging consumed 19% of gross income in FY24, when EUR exposure was approximately 45% of NAV. With EUR exposure now at 70% (April 2026), the hedging burden on the remaining non-EUR book is proportionally smaller, and the forward drag should moderate, though the actual impact will depend on the currency mix of new originations and prevailing hedging costs.

2.13. Industry Overview & Market Context

SME defaults in Europe have been on a multi-year climb following the withdrawal of post-COVID support measures, driven by tighter financial conditions, elevated input costs, and slower economic growth. The default increase observed in GDADF is consistent with this broader credit cycle trend across European jurisdictions and sectors, and remains in line with historical experience and within the structural absorption capacity of the portfolio. Recent dynamics have also been characterised by slightly lower recovery rates on smaller, highly granular trade receivable exposures, where the cost-benefit of pursuing recovery may favour earlier write-off. More recently, there are signs of stabilisation, with defaults potentially approaching cyclical peaks, suggesting the mature stage of the credit cycle. Management’s outlook is for moderation or decline in defaults over the medium term, supported by the portfolio’s short duration, high granularity, credit enhancement, and quality of the underlying assets. Fasanara leads the competitive landscape at USD 6Bn AUM versus USD 3Bn for the next competitor, with 141 integrated platforms. Several named competitors have experienced fund shutdowns or trading significantly below par. Fasanara’s proprietary technology stack was validated by Blackstone’s 20% acquisition of the spun-off technology entity.

Qiro Lens: GDADF’s structural defences - bankruptcy-remote SPVs, originator-excluded collections, senior-first waterfall are genuine and well-documented. The 60-90-day portfolio duration means the book self-liquidates within 2-3 quarters through natural run-off, providing an inherent liquidity backstop that was stress-tested during COVID-19 (zero negative monthly returns throughout). The rising default trajectory (0.5% → 1.17%) warrants monitoring but remains well within the fund’s structural absorption capacity.

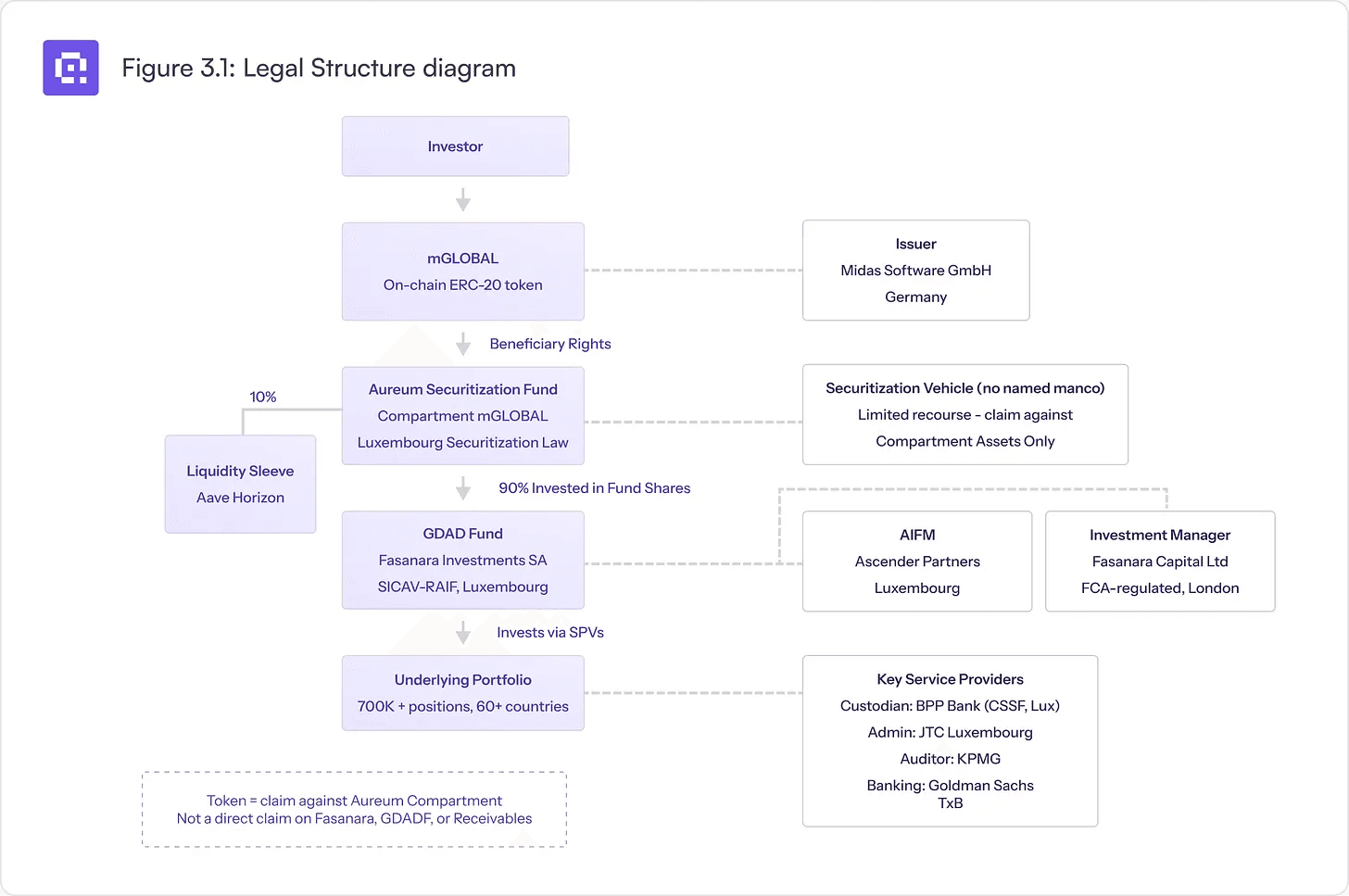

Section 3 - mGLOBAL Legal Structure

3.1. Legal Construct

The mGLOBAL token is issued by Aureum Securitisation Fund, acting through a dedicated compartment (Compartment mGLOBAL), under Luxembourg securitisation law. Midas acts as the tokenisation and platform layer but is not the legal issuer. The token represents a legal claim against the Issuer/Compartment - not a direct claim against Fasanara Capital, the GDADF sub-fund, or the underlying receivables.

To be explicit, mGLOBAL token holders do not have the same legal rights as direct subscribers into the GDADF fund. A direct fund investor holds fund shares directly, whereas mGLOBAL token holders have a claim against the Midas Compartment (an SPV), which in turn holds the fund shares. This introduces an additional legal layer between the token holder and the underlying fund.

Figure 3.1: Legal Structure diagram

3.2. Investor Protection

mGLOBAL token holders benefit from several layers of legal and structural protection. First, the Aureum Securitisation Compartment is legally ring-fenced losses or liabilities of other Aureum compartments cannot affect the mGLOBAL compartment’s assets.

Second, the beneficiary rights structure ensures that if Midas Software GmbH were to become insolvent, token holders retain their claim against the Compartment assets rather than becoming unsecured creditors of Midas. Third, the GDADF shares held by the Compartment are protected by the fund-level structural protections described in Section 2.11.

Recourse is limited to the Compartment, which is standard for securitisation structures and reflects the underlying investment risk rather than an additional structural weakness. A structural subordination point warrants attention: Conditions 3 and 8.2 of the mGLOBAL T&Cs make the Notes subordinate to the Units in the Priority of Payments, stating that investors have recourse only to the assets of the Compartment remaining after satisfaction in full of the claims of the Unitholders. This appears to invert the default Luxembourg SecAct 2004 practice, where notes typically rank senior to units.

In a severe stress scenario where the Compartment’s GDADF shares are impaired and the liquidity sleeve is depleted; token holders bear the loss. The OTC L3 facility (USD 130M) provides a backstop but is not a guarantee.

3.3. Layered Claim Structure

mGLOBAL holders are four layers removed from the cash-generating assets: the token represents a claim against the Compartment, which holds GDADF shares, which hold SPV notes, which hold the underlying receivables. Each intermediary layer introduces its own legal, operational, and timing dynamics but also serves a distinct creditor-protection function: compartment ring-fencing isolates mGLOBAL assets from other Aureum liabilities, fund-level governance provides independent oversight, bankruptcy-remote SPVs protect against originator insolvency, and receivable-level collateralisation secures the underlying cash flows. In a severe stress scenario, enforcement of claims must traverse each layer sequentially, potentially resulting in delays, legal costs, and recovery haircuts that would not affect a direct holder of the underlying receivables.

3.4. Regulatory Landscape

Tokenised securities sit in an evolving regulatory landscape. Changes in Luxembourg securitisation law, EU Markets in Crypto-Assets (MICA) enforcement, or jurisdictional treatment of tokenised notes could affect transferability, tax treatment, or legal enforceability of token holder claims. The interaction between traditional securities regulation and on-chain token transfers creates jurisdictional ambiguity - particularly for secondary market transactions where token holders may reside in jurisdictions with different regulatory frameworks. Regulatory developments across the EU, UK, and key investor jurisdictions continue to evolve.

Qiro Lens: Each legal layer adds genuine protection and enforcement distance. mGLOBAL holders hold a claim on a claim on a claim: structurally sound, but remedies traverse four layers sequentially. The ring-fencing at Compartment and Sub-Fund level is credible under Luxembourg law, though untested for tokenised securitisation notes in a cross-border insolvency scenario.

Section 4 - mGLOBAL Technical Structure

4.1. Midas Platform Overview

Midas Software GmbH serves as the tokenisation and platform layer for mGLOBAL. Midas handles the minting and burning of tokens, USDC custody during subscription windows, fiat off-ramping to the Compartment’s bank accounts, and the $93/7$ NAV reconciliation process. While Midas is not the legal issuer (the Aureum Compartment is), it is the operational layer through which all token lifecycle events flow. Any disruption to Midas’s operations - whether through insolvency, regulatory action, or technical failure - would impair subscription and redemption functionality even if the underlying GDADF continues to perform normally.

4.2. Smart Contract Architecture

mGLOBAL is deployed as an ERC-20 token on the Ethereum blockchain. The smart contract governs token minting, burning, transfers, and the on-chain representation of NAV. Key structural features include the audit status and scope of the smart contract code, the presence of upgradeability mechanisms (proxy patterns) that could allow contract logic to be modified post-deployment, and the existence of privileged roles (admin keys, pause functions, blacklist capabilities) that concentrate operational control. These are standard diligence items for any tokenised product. Midas has published independent third-party security audit reports for its smart contracts (available at docs.midas.app/resources/audits). As with any upgradeable contract system, ongoing audit coverage and periodic re-assessment remain important.

4.3. Oracle & NAV Feed Mechanism

The on-chain NAV for mGLOBAL is updated monthly, based on the official NAV published by JTC Luxembourg. This creates a structural latency: between updates, the token’s on-chain price reference reflects a stale valuation. In a rapidly deteriorating credit environment, the on-chain NAV could materially overstate the true value of the underlying portfolio.

The $93/7$ subscription and redemption mechanic serves as a specific anti-dilution and stale-NAV mitigant: only 93% of tokens are delivered or redeemed immediately, with the remaining 7% reconciled after the official JTC NAV is published, protecting existing holders from dilution between valuation dates. While some residual information asymmetry remains between updates, this holdback mechanism materially narrows the window for adverse selection. The oracle update mechanism, its trust assumptions (who can update the price, what safeguards prevent manipulation), and fallback procedures in the event of oracle failure are critical infrastructure components that benefit from independent technical review.

4.4. Admin Key & Upgrade Controls

ERC-20 token contracts typically include administrative functions such as pausing transfers, blacklisting addresses, minting new tokens, or upgrading contract logic. The distribution and security of these administrative keys is a material structural factor. Admin key controls govern minting authority, transfer pausing, and oracle updates the security architecture around these functions determines the practical enforceability of the token’s design. Best practice requires multi-signature wallets with geographic and organisational distribution, hardware security modules (HSMs), time-locked governance actions, and transparent on-chain governance processes. The key management architecture for mGLOBAL has not been independently reviewed for this report; allocators may wish to request disclosure of multisig composition, timelocks, and audit reports.

4.5. Blockchain Infrastructure

As an Ethereum-based token, mGLOBAL is exposed to blockchain-level risks including network congestion (which can delay or increase the cost of transactions during stress events), consensus-level vulnerabilities, and the evolving Ethereum roadmap. Gas fee spikes during market stress could make small redemptions economically unviable. The token’s dependence on Ethereum’s continued operation and security is a foundational assumption worth noting. Additionally, any bridge risk introduced by cross-chain deployments or L2 integrations would compound the technical attack surface.

4.6. Stablecoin Dependency

The mGLOBAL structure depends on USDC as the primary stablecoin for subscriptions, the liquidity sleeve, and instant redemptions. This creates a material dependency on Circle (the USDC issuer) and its banking partners. A USDC depeg event as observed briefly in March 2023 following the Silicon Valley Bank collapse - would simultaneously impair the value of the liquidity sleeve, disrupt instant redemption mechanics, and potentially create a NAV discrepancy between the on-chain and off-chain valuations. Concentration of stablecoin exposure in a single issuer amplifies this risk relative to structures that diversify across multiple stablecoin providers.

Qiro Lens: The technical layer is where mGLOBAL’s structural profile diverges most from the underlying fund. Smart contract audit status, admin key distribution, and oracle update frequency are foundational infrastructure choices that shape the token’s practical behaviour. The on-chain NAV is derived from the official monthly JTC valuation, with Midas applying an intermediate update process that includes internal cross-referencing against independent data sources, oracle-level tolerance checks, and dual co-signer review before each price push. While this multi-layered process narrows the staleness window, the underlying JTC NAV remains a monthly input the on-chain price between official prints is an internally validated estimate, not a market-observed value. Allocators should understand the distinction between update frequency (how often the price moves on-chain) and source frequency (how often the underlying portfolio is independently valued).

Section 5 - mGLOBAL Subscription & Redemptions

Note: the subscription process below describes the mGLOBAL on-chain route. Direct GDADF subscriptions follow a separate monthly cycle with 15 days’ notice as described in Section 2.1.

5.1. Subscription Flow

Step 1: The investor deposits USDC into the Midas minting vault (requires prior KYC/AML greenlisting); the monthly window opens 6 business days before month-end and closes 3 business days before Valuation Day.

Step 2: The investor deposits USDC into the Midas minting vault (requires prior KYC/AML greenlisting); the monthly window opens 6 business days before month-end and closes 3 business days before Valuation Day.

Step 3: When mGlobal tokens are minted, 90% of deposited USDC is off-ramped by Midas and subscribed into the underlying GDADF Fund, with NAV pricing based on the last calendar day of the month. The remaining 10% is allocated to the liquidity sleeve supporting instant redemptions.

Step 4: The remaining 7% of tokens are minted and airdropped after the new official month-end NAV is published by JTC Luxembourg (typically by the 20th of the following month); the final token count is reconciled against the effective NAV price.

Note on 93/7 split : It is timing-driven, the official month-end NAV for GDADF is typically not finalised until approximately the 20th of the following month. Rather than delaying token delivery for several weeks, Midas mints on the last known NAV and delivers 93% immediately. The 7% holdback serves as a buffer against potential NAV discrepancy. Once the official NAV is published by JTC, a true-up is performed and the remaining 7% is delivered at the corrected price. The same logic applies in reverse for redemptions.

5.2. Redemption Pathways

mGLOBAL offers four redemption routes - two instant (L1 and L2), an OTC secondary exit (L3), and a standard monthly redemption each representing an independent choice available to the token holder. The routes operate across a tiered liquidity waterfall, sequenced below from fastest to slowest:

Figure 5.1: Redemption Waterfall

Table 5.1: Redemption Waterfall Details

The facility operates on a discretionary basis, not a commitment. In practice, approximately $5-10M is available on an as-needed, same-block basis. InfiniFi deploys liquid reserves for siUSD, then unwinds short-term positions in stablecoins like PYUSD or USDG to refill liquidity. The capacity is dynamic and fluctuates with InfiniFi’s overall deposit base. The headline $30M figure cited during the Aave onboarding process was the committed amount at the time of due diligence; the actual available instant liquidity at any given point is significantly lower.

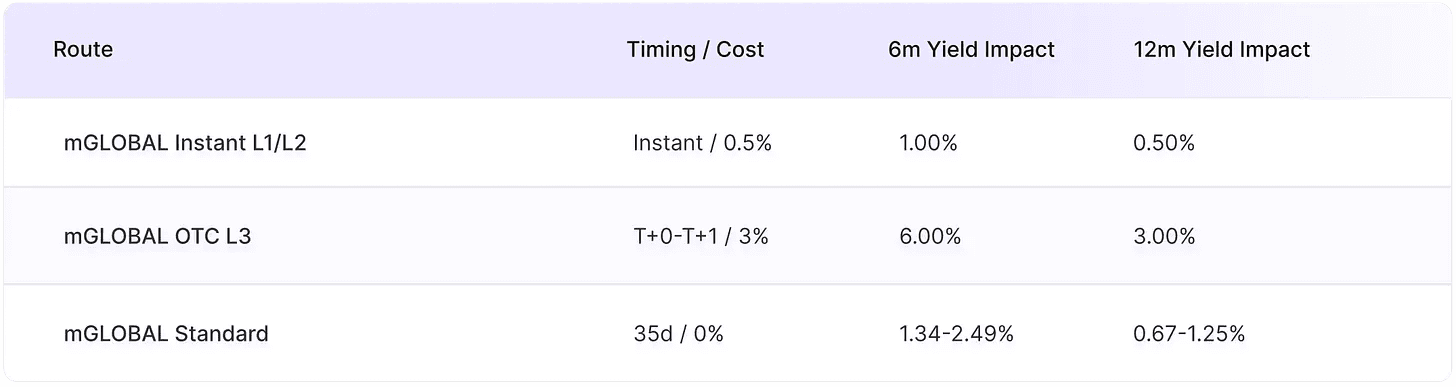

*mGLOBAL Standard redemption is processed on a monthly cycle and is expected to settle in 35 days where the request is submitted within the relevant monthly cut-off. Timing may extend (up to 65 days) where a request misses the applicable cut-off and rolls into the following monthly cycle.

Table 5.2: Estimated annualised yield drag (assuming 7% net annual yield):

Yield drags calculated as foregone yield during the notice-to-settlement period, annualised relative to holding period.

Key Observation: At a 12-month hold, route selection alone produces a 0.50%-3.00% dispersion in realised yield. At 6 months, the range widens to 1.00%-6.00%. mGLOBAL Instant L1/L2 sits at the efficient end of the spectrum for holding periods beyond 6 months.

Note that L1 capacity is proportional to TVL while L2 (USD 20M) and L3 (USD 130M) are fixed-dollar. At low TVL, L2 alone may exceed L1; at high TVL, all fixed-dollar facilities become marginal relative to the base.

5.3. Redemption Considerations

Liquidity Sleeve Depletion: If instant redemptions exceed 10% of TVL, L1 is exhausted. L2 provides only USD 20M of backup. Beyond that, investors fall back to the OTC route (3% haircut) or the 35 day Standard route. In a correlated stress scenario where multiple holders seek to exit simultaneously all three on-chain routes could be effectively capacity-constrained at the same time, leaving only the standard monthly redemption (35 days) route available.

Redemption Timing Asymmetry: For instant redemptions, yield stops accruing upon acceptance and the token is subject to potential holdback adjustment. For standard monthly redemptions, yield continues to accrue until the next Valuation Day (month-end NAV). Settlement timelines range from near-instant to 35 days depending on the route. The yield treatment difference is worth factoring into expected returns, particularly for shorter holding periods. The settlement window is broadly in line with other tokenised private credit products, though allocators should benchmark against specific comparable structures.

Midas Operational Dependency: All mGLOBAL redemption routes flow through Midas’s platform infrastructure. An operational disruption at Midas would impair redemption processing even if the underlying GDADF and Aureum Compartment are functioning normally. This single-point-of-failure risk at the platform level is not mitigated by the legal ring-fencing that protects against Midas insolvency.

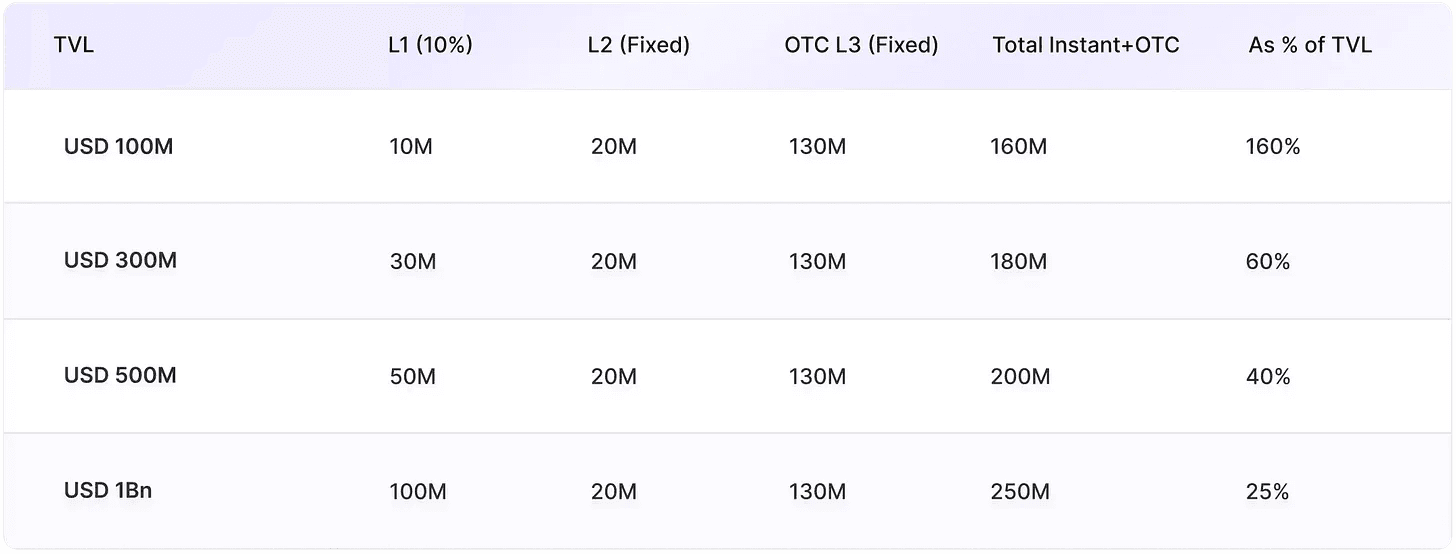

Table 5.3: TVL Liquidity Scaling

Key Observation: Liquidity should be assessed as a multi-layer waterfall, not only through the 10% instant sleeve. L1 scales with TVL; L2 (USD 20M) and L3 (USD 130M+) are fixed-dollar. The standard monthly route (35 days) provides full-capacity exit for all holders. As TVL grows, instant-exit coverage shrinks in percentage terms, but the total waterfall remains substantial. Allocators should size positions with reference to the full liquidity stack.

Section 6 - mGLOBAL DeFi Composability

6.1. DeFi Lending Market Integration

mGLOBAL is designed for composability across on-chain DeFi lending markets, with Aave as the current primary integration venue. The L1 liquidity sleeve deposited in the lending market serves a bounded liquidity management function supporting subscriptions and redemptions - rather than operating as a separate return-seeking DeFi strategy. The sleeve can be governed through permitted asset and protocol eligibility limits. The LTV ratio set by the lending market’s governance determines the maximum achievable leverage multiple.

Aave Protocol Considerations: Depositing the liquidity sleeve in Aave introduces DeFi protocol risk. A smart contract exploit, governance attack, or liquidity crisis in the lending market could lock or impair the sleeve - precisely when instant redemptions might be most needed, as stress events tend to be correlated across crypto markets. The liquidity sleeve is designed as the first line of defence for redemptions; housing it within a third-party DeFi protocol creates a dependency that could fail under stress.

6.2. DeFi Composability Considerations

The following dynamics are inherent to any tokenised private credit asset used as DeFi collateral. They are best managed through protocol-level parameter calibration rather than treated as impairments of the underlying asset.

Leverage Cascade Dynamics: If leveraged mGLOBAL positions are liquidated en masse triggered by an NAV decline, oracle update, or broader market stress forced selling could drain the liquidity sleeve, trigger OTC facility drawdowns, and create selling pressure that exceeds available on-chain liquidity. This dynamic can affect redemption capacity for all mGLOBAL holders, making LTV limits, supply caps, and borrower concentration controls critical calibration points for any lending market integration.

Maturity Mismatch: DeFi borrowing is typically short-term and callable, while the underlying GDADF portfolio has 60-90-day duration and quarterly redemption gates. A leveraged borrower who is liquidated cannot atomically redeem the underlying mGLOBAL beyond the 10% sleeve. This maturity mismatch means that during a liquidation cascade, the on-chain market price of mGLOBAL could trade at a discount to NAV. Protocol-level utilisation monitoring and liquidation design can bound this risk but cannot eliminate it entirely.

NAV Oracle Dynamics: The monthly NAV update creates a window where informed participants may have superior information about the true value of the underlying portfolio. In DeFi lending markets, the oracle price determines liquidation triggers - a stale NAV that overstated value could delay necessary liquidations, while a sudden correction could trigger unnecessary cascading liquidations. The interaction between infrequent NAV updates and real-time DeFi liquidation mechanisms is a structural tension inherent to tokenised private credit products used as DeFi collateral.

Qiro Lens: DeFi composability is simultaneously mGLOBAL’s strongest differentiator and an area requiring careful protocol parameterisation. Leverage, liquidation, and maturity-mismatch dynamics are collateral-parameter considerations - managed through LTV settings, supply caps, borrower concentration limits, liquidation design, oracle configuration, and utilisation monitoring rather than fundamental impairments of the underlying asset quality. The looping strategy amplifies returns for leveraged participants but can affect redemption capacity, making protocol-level risk parameter calibration essential for all DeFi lending market integrations.

Section 7 - Key Observations

mGLOBAL Structure at a Glance - How the investment stack connects from investor to underlying receivables

Figure 7.1: mGLOBAL Structure at a Glance

7.1. Strengths

Securitisation structure with bankruptcy-remote SPVs providing credit isolation from fintech originators; no direct lending exposure.

Credit enhancement via originator first-loss (5-30% skin-in-the-game) and credit insurance covering 75% of portfolio.

Conservative concentration limits well within PPM maximums.

90% institutional investor base providing capital stability.

No negative monthly return since inception (September 2017) across multiple stress events.

Gross 9.01% CAGR since inception with ultra-low volatility.

Blackstone technology partnership validating institutional-quality platform.

Short 60-90 day duration providing natural hedge against rate and credit cycles.

Strong service provider network: Goldman Sachs, KPMG, JTC, BPP Bank.

7.2. Challenges

Rising default trajectory: 0.5% (2022) → 1.17% (2025), though FY26 YTD moderating to 0.34%, driven by SME credit cycle pressures.

Redemption yield drag: for instant redemptions, yield stops accruing upon acceptance; for standard monthly redemptions, yield accrues until next Valuation Day.

FX hedging cost consumed 19% of gross income in FY24.

Geographic concentration: UK+US = 38% of NAV; currency concentration in EUR (70%) and GBP (16%).

20 originators discontinued since inception; reliance on backup servicer arrangements.

Lean 3-person Board for a USD 6Bn firm.

Internal credit ratings (FDR) - not externally verified at individual debtor level.

7.3. mGLOBAL-Specific Considerations

In addition to the GDADF level risks above, mGLOBAL investors are subject to tokenisation-layer factors that are absent from the direct GDADF route. These include smart contract vulnerabilities and admin key risks; Midas operational dependency as a single point of failure for token lifecycle events; USDC stablecoin concentration risk; DeFi lending market protocol risk affecting the liquidity sleeve; monthly NAV oracle staleness and adverse selection; liquidity sleeve depletion risk under correlated redemption pressure; leverage cascade risk from DeFi composability; maturity mismatch between DeFi borrowing and underlying fund liquidity; regulatory uncertainty across EU/UK tokenised securities frameworks; and the layered claim structure placing investors four steps from the underlying cash flows. These factors represent the trade-off accepted for on-chain accessibility, transferability, and enhanced liquidity relative to direct GDADF subscription.

7.4. Key Takeaways

The Fasanara GDADF (USD 1.14bn, sitting within Fasanara’s broader USD 3.5bn ABF / receivables platform) exhibits a robust structural framework complemented by a track record dating to September 2017. The combination of bankruptcy-remote SPV structures, originator first-loss provisions, credit insurance, conservative advance rates, and extreme diversification (700,000+ positions) has delivered a gross 9.01% CAGR with zero negative monthly returns - a record that few private credit funds can match.

The collections architecture is institutionally sound: Fasanara-controlled Goldman Sachs accounts with originator-excluded access, senior-first waterfall priority, and monthly payment cycles provide credible structural credit protection at the cash-flow level. The 17.1% average attachment point for senior tranches, combined with the fund’s 60-90-day portfolio duration, means the book self-liquidates rapidly through natural run-off, providing an inherent liquidity backstop.

However, the default trajectory and the FX hedging cost drag (19% of gross income) represent the primary areas of ongoing attention. The fund’s clean record is structural but it requires ongoing discipline in originator selection, concentration management, and the maintenance of credit enhancement coverage as the book scales toward USD 1.5Bn.

The mGLOBAL tokenisation layer introduces a distinct set of risks that sit on top of the underlying credit profile. While the legal structure Luxembourg securitisation compartment with ring-fencing and beneficiary rights provides credible investor protection, the technical infrastructure (smart contract security, oracle mechanisms, admin key controls) and operational dependencies (Midas, DeFi lending markets, USDC) have not been independently verified for this report and represent areas where Qiro’s credit curation framework adds value. The DeFi composability features that make mGLOBAL attractive - instant redemptions, on-chain transferability - simultaneously introduce structural dynamics (leverage cascades, liquidity sleeve interaction, maturity profile) that are relevant to all token holders during periods of elevated activity. The convenience and liquidity benefits of the tokenised wrapper are best weighed against these additional layers when evaluating mGLOBAL relative to direct GDADF subscription.

For protocols and institutional investors considering on-chain deployment into mGLOBAL, Qiro Finance provides bespoke underwriting, risk parameter calibration, and ongoing monitoring services. Our credit curation framework evaluates the full investment stack from underlying receivable quality through to smart contract infrastructure enabling informed allocation decisions tailored to specific portfolio constraints and risk appetites.

About Qiro Finance

Qiro Finance - Private Credit Curator for DeFi

Qiro is a private credit curator for DeFi - the allocation partner for protocols, vaults, and treasuries deploying capital into tokenised private credit. Curation goes beyond risk assessment: Qiro helps allocators select and underwrite opportunities, structure and deploy capital, actively manage exposures through the life of each position, and continuously monitor risk - so allocators capture private credit yield with institutional discipline, without building a credit team in-house.

Qiro’s curation framework spans the full capital lifecycle:

Sourcing & Credit Assessment: Institutional underwriting of every opportunity before deployment: data room review, credit appraisal, quantitative risk scorecard, and formal approval.

Capital Deployment & Structuring: Risk parameter setting, exposure limits, collateral and covenant frameworks, and concentration controls calibrated to each allocator’s mandate, with capital deployed only once conditions precedent are met.

Active Portfolio Management: Ongoing oversight of deployed capital: daily accrual-based NAV, rebalancing inputs, and exposure management as portfolios evolve.

Risk Monitoring & Reporting: Continuous tracking against defined trigger conditions, structured escalation on breach, and periodic risk reporting for investors and governance.

Deploying capital into tokenised private credit? Partner with Qiro for end-to-end private credit curation - sourcing, underwriting, deployment, and monitoring.

Contact: Qiro Finance

Email: akshay@qiro.fi, nishikant@qiro.fi

Website: https://www.qiro.fi

Twitter: https://x.com/Qiro_Finance

LinkedIn: https://www.linkedin.com/company/qiro-finance/

Disclaimer

This document is prepared by Qiro Finance for informational purposes only. It is based on publicly available information and materials made available by the fund manager and token issuer, which Qiro believes reliable but has not independently audited. It does not constitute a commissioned underwriting opinion, investment advice, or an offer or solicitation to buy or sell any securities, fund interests, or digital assets in any jurisdiction. This document is not directed at U.S. persons or at any person in a jurisdiction where its distribution would be unlawful. Past performance is not indicative of future results, and forward-looking statements involve assumptions that may prove incorrect. Recipients should conduct their own due diligence and consult their own legal, tax, and financial advisers before making any investment decision.